Tl;dr: We are going to learn what preference shares are and that they are different from what you, the founders and your staff get.

I was emailed by a founder who asked the naïve question “Can we just give common shares to investors? Why do we need to give preference shares?”

I’m pretty sure a lot of people don’t have a clue about preference shares, so let’s clear this up for you now. Don’t worry, no one was born knowing everything. You need to learn.

What are preference shares

When an investor invests in your startup they are given a share certificate in return. They, therefore, own a share of your company legally. There are two types of shares (AKA “stock”):

- Common shares: This is what founders have and start with. You issue your staff options and they turn into common. You have no real special rights (If you negotiate super-voting rights like you read Mark and Evan had, these are a special kind of share class and not normal). One share is the same as all others. Also, there is no such thing as ‘founder shares’, btw.

- Preference shares or stock: This is a different ‘class’ of shares to common shares. This is what investors get. They’re special, sort of why they are also called ‘preferred stock’. One way to think about preferred shares is like debt with no interest, but repayment happens on exit since there are features you might understand from getting a mortgage. When you create this new class of shares, certain rights and privileges are afforded to them. There is a list of potential rights which we will discuss later.

It is worth understanding that in every new round of investment there will most likely be a new ‘class’ of preferred or preference share which will be issued. Like going up a waterfall, each new class is ranked higher than the other and the money water splashes on them first. When you exit your startup and the water gushes out with cash, the water flows down with the latest class of investor stock getting first dibs on it. You, the founders with common stock are at the bottom of the waterfall, hoping a huge pool will be made, not a barren swamp.

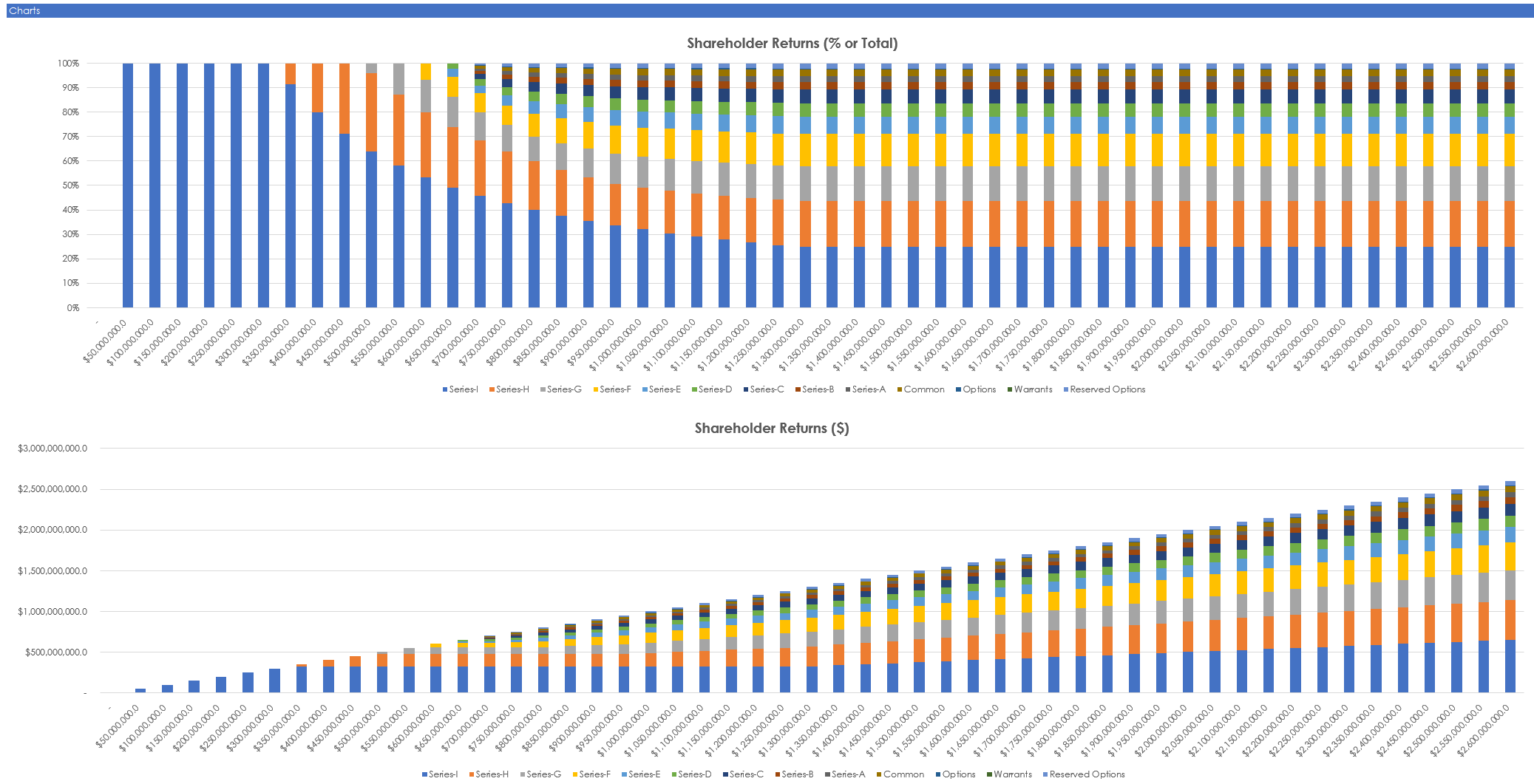

Here is an example from my cap table returns analysis. You can see it starts all blue and then fades down over time. The blue is Series-I preference shares and the orange is Series-H. The small brown bar near the top is common stock… what the founders have.

The top graph is a % of the total return and the bottom graph is the dollar return that is paid out. You totally will expect to get more, this is just a random example I made for illustration purposes.

Where does the name come from?

Preference shares or again… preferred stock’s etymology is from ‘liquidation preference’. There is a preference baked in.

The first preferred stocks were issued by railroad companies and canals in the mid-1800s who wanted to sweeten deals to get the funding they wanted.

Why do investors want preference shares?

In short. your startup has three outcomes:

- Do super well (Rare)

- Do ok, or (A few)

- Die (most)

Die. Most startups go the way of the dodo, and investors know this. No one is getting something.

OK. Some companies raise a lot of money and get a meager outcome. There is something and investors want it all.

Super well. When you kill it, this liquidation stuff doesn’t matter that much as it’s bottles and models for everyone. Investors don’t take their preference, they convert to common and take their fair share (unless they have participating preferred and they get both their investment and their unfair share).

It’s the middling outcomes that investors are optimizing the downside for, the OK ones. They want to make sure they get their money back whenever they can.

Assuming you have a 1x liquidation preference, the liquidation preference is the value of their initial investment, the capital invested is what they hope to protect (Investors like to make money but they hate to lose it!). If the investor invests $10m, their liquidation preference is worth $10m (a 2x one is worth $20m and so on). If the investor invests $10m at a $30m pre-money valuation they effectively own 25%. They decide if they convert to common and take 25%. If you are worth $40m, their converted value is the same as their preference- $10m, so they do either. It doesn’t matter. If you sell for $35m they are taking their preference.

A liquidation preference gives investors an option to choose what they want to do in all of those three scenarios assuming there is some kind of residual value. They can take their money back or they can convert to common and take their ownership stake. A preference sets a cap on the amount they can get instead of if they convert. So if you have one investor who chucked in $10m and you sell for $10m… they take the preference and take it ALL. You don’t get a dime. I’m serious. Feck all! You’re broke again.

So what happens in the three scenarios (I’m keeping this simple for you!):

- Do super well: So you get an offer from Facebook and sell for $100m. The investor’s stake is worth $25m. Their preference is worth $10m, so they want to take $25m instead of $10, right?

- Do ok: Now this is where things get scary for founders. You sell for $9m to Yahoo. That’s now bad, right? $9m will get you a Tesla, or ten! But… the liquidation preference is $10m. Their shareholding (on ‘as converted’ basis) is worth a bit more than $2m. So what happens? Yes, they take ALL the $9m and founders get nothing

- Die: Whatever happens, any value is going to the investors. When you enter bankruptcy the investors at the top of the preference stack get paid, and it pays out down the waterfall such that a lower down VC may get nothing. This filters through the preference investors until you hit common (you)

Is this normal? Do you have to provide them?

Yes. Why have common shares when you can be preferred? They are the norm. Terms change over cycles, but not so much vanilla preferences.

It’s really suuuper uncommon for investors, especially at series-A and after not to have preference shares.

What about convertible notes, you may be wondering? They typically convert into the same class of share at the point at which they convert. So if you do a CN and then seed, then CNs get the same as the seed investors.

- Venture capitalists: With few exceptions, all VCs will require you to issue them preference shares

- Angels: Many or most will also expect preference shares. It depends on their level of sophistication, but typically they model themselves on VCs so they will copycat

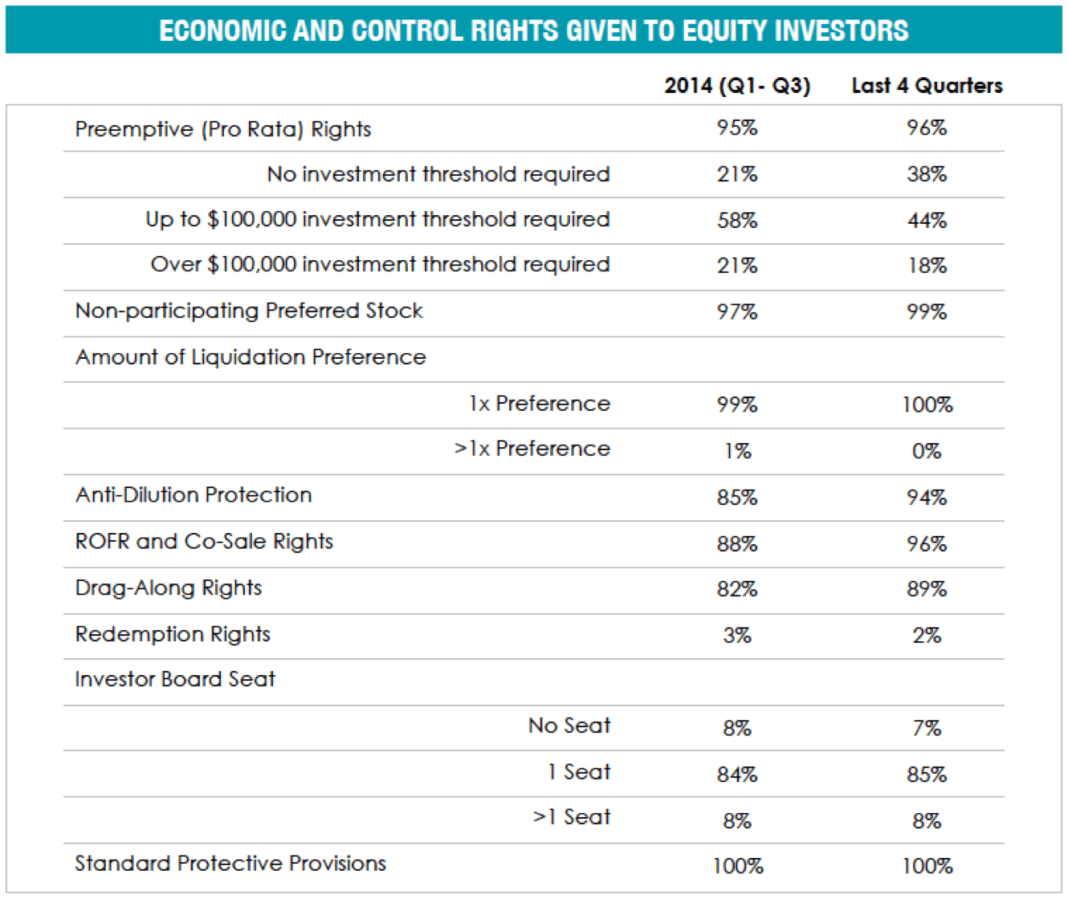

Here is a table from research to tell you what is normal. You can read more about what venture capital terms are standard here.

The answer you are looking for in preference share is under ‘non-participating preferred stock‘. It’s 97-99%!

Screw you, I am the chosen one

Yes, everything is negotiable, but don’t be delusional. You need to be hot shite to get what you want. The most known examples are Facebook, Google and Snapchat. That’s the league you need to be in to start dicating terms.

If you are hot shite, negotiate. If you are not, don’t piss people off. Naked people have little to no standing in society.

Are preference share ever beneficial to you?

Generally no, but also yes. But for two uncommon reasons, you would not think about.

Firstly, there is actually a fab reason as to why you want to have preference shares. For your staff’s benefit. If investors pay $1 for preference shares that is a different class of stock. They haven’t changed the price for common shares in a manner. If your options are worth 25 cents per share, you can still issue options at this lower price which means more upside for staff. Their ‘fair market value’ is lower. If the investors had bought common shares the value for all new staff would be commensurately higher.

Secondly, this is not really an obvious benefit prima faces but it is worth bearing in mind. Typically your main investors have a Board seat. The board owes a ‘greater fiduciary responsibility‘ to common shareholders over preferred investors who are deemed to be unsophisticated. So put another way they are legally required to ‘prefer’ (is that a joke?) common over preferred (investor) stock when making decision. No comment if that actually happens.

What terms come along with preference shares?

These issues receive preference over all other classes of the company’s preferred (except for prior preferred). If the company issues more than one issue of preference preferred, the issues are ranked by seniority. One issue is designated first preference, the next-senior issue is the second and so on.

Here are the main categories of terms that require a preference class to be created over common:

- Dividends: Do you pay dividends ‘when’ you earn enough money to make them (typically if you are a public company). They can be cumulative and non-cumulative. Cumulative means they keep adding up each year on whatever you offer them. Dividends can also be fixed and adjustable (Prefered shares matter more for public companies in this context)

- Callable: You have the right to buy back the preference shares from investors at a predetermined price and date. This can decrease the value of a share issuance wince you restrict the upside potential of share appreciation. The call option can be for a term or perpetual

- Convertible: The investor has the right, but not the obligation to convert their preferred shares to common shares at a conversion ratio. They will either take their preference or convert it to common depending on what is worth more.

- Participation: When you sell, the investor gets their money back AND they get their equity upside (This is not common. Like 1% of deals. More happens for late stage deals where there is some risk, or super-high price)

- Voting and non-voting: Do the preference shareholders have a right to vote on corporate matters, including those on payment on dividends?

- Anti-dilution: This exists, but is not common. I’m going to mention it anyway. An anti-dilution clause means that once investors invest, they don’t get diluted in future rounds. I honestly would tell investors to go feck themselves

What are the types of preference shares?

There are in fact many different types of preference shares. The naming convention stems from the type of liquidation preference they have.

Here are the four main flavors:

- Convertible preferred stock: This is your bog standard preference share. They can either get their investment back (preference) or convert to common shares ‘as converted‘ and take the $ ownership they have

- Participating preferred stock: Owners of preferred shares double dip when you exit. You pay the investors the money they invested AND then they also take their share on an ‘as converted‘ basis. Let’s say they invest $20m for 20% and you exit for $100m. The investor gets 20m (participation) plus $20m (Their 20% preference, though they can also convert), so $40m.

- Non-cumulative preferred stock: Unlike cumulative preferred stock, dividends will not accumulate if they are unpaid. You can choose not to pay dividends and shareholders have no right to make you issue dividends

- Cumulative preferred stock: This adds on dividends. You need to pay your preferred shareholders dividends, but there is a catch. If you don’t pay a dividend, it will accumulate and need to be paid in the future. In such circumstances, common shareholders receive no dividends till the preferred shareholders have been paid up

There are a few types of liquidation preference:

- Multiple liquidation preferences: A 2x liquidation preference means their threshold is $20m using the example above ($10m investment). This may also include accrued and unpaid dividends if agreed.

- Participating preferred: This is pretty nasty. The investor gets his cake and eats it too. They get the $20m PLUS their 25% stake. This may also include accrued and unpaid dividends if agreed again as above. Participating preferred stock is favored by investors because they will receive a preferential return over both low and high exit transaction values (Best to negotiate for a cap if you have to accept this preference. Yes, you can cap participation but this starts getting even more technical).

- Screw you: The ultimate screw you is multiple participating, cumulative, convertible, non-callable, voting, anti-dilutive liquidation preference.

How do you make preference shares?

Simply put, your lawyer will deal with all this. You tell them what the terms are, or the terms in detail are negotiated when you finalize your shareholder agreements with you investor and their lawyers. Your articles of association have to be updated to reflect the preference shares and this is where all the rights of the preference shares live and can in future be read and understood. Your lawyer will issue the investors a share certificate for preference shares.

What happens to preference shares when you exit?

Great, so you are going to exit! Congrats. Now what?

Simply put, investors decide what they want to do according to the rights they have with their preference shares. This is mainly to do with their type of liquidation preference. Whilst the details can get complicated (particularly calculations) the high level is pretty basic.

If holders of common stock would receive more per share than holders of preferred stock upon a sale or liquidation (typically where the company is being sold at a high valuation), then holders of preferred stock should convert their shares into common stock and give up their preference in exchange for the right to share pro rata in the total liquidation proceeds.

If investors don’t want to convert their stock into common, they take their preference and common shareholders get what is left. In the case of participating preferred the investors do a similar decision, but in any case, they get their liquidation preference first.

Please note that each series of preferred stock may be economically incentivized to convert to common stock at different transaction values due to different preference amounts per share for the different series. This necessitates creating complex spreadsheets to model what happens upon a sale of the company at different transaction values. The most sophisticated spreadsheets will also take into account whether options and warrants are in the money at certain transaction values, which will affect whether or not they are exercised, which will then affect the price per share.

Conclusion

Yes, this stuff can get crazily complicated, so don’t attempt these negotiations unless you know a lot!

If you want commercial advice on term sheets, reach out to me. If you don’t have a VC lawyer and are looking for one, reach out and I can recommend lawyers in different countries that can be on your side and help you not get screwed over. A good lawyer who knows this shizzle is important. I’m serious. Don’t cheap out here.