It used to be the case that the big VCs made all the returns and because of this ostensible fact, were able to charge ‘premium fees’ of 2.5-3% and be highly selective in whom they allow to be their LPs. This is a notion I am sure is perpetuated for obvious reasons, only now, it doesn’t seem entirely accurate. Something that will be music to the ears of emerging funds.

“the widely held belief that 90% of venture industry performance is generated by just the top 10 firms is a catchy but unsupported claim that may lead Lps to miss attractive opportunities with managers that can provide exposure to substantial value creation.”

Research posted by Cambridge Associates (“CA”) in November of 2015 paints a changing picture of the venture capital fund landscape. This is not to say it is clear-cut, but the underlying trend is becoming evident.

CA analysed the top 100 venture investments by value creation (i.e. total gains) between 1995 to 2012, an 18-year period, and found, in summary:

- an average of 83 companies each year account for value creation in the top 100 investments in the asset class for each year;

- in the post-1999 (i.e., post-bubble) period, the majority of the value creation in the top 100 each year has, on average, been generated by deals outside the top 10 deals;

- an average of 61 firms account for value creation in the top 100 investments in venture capital per year; and

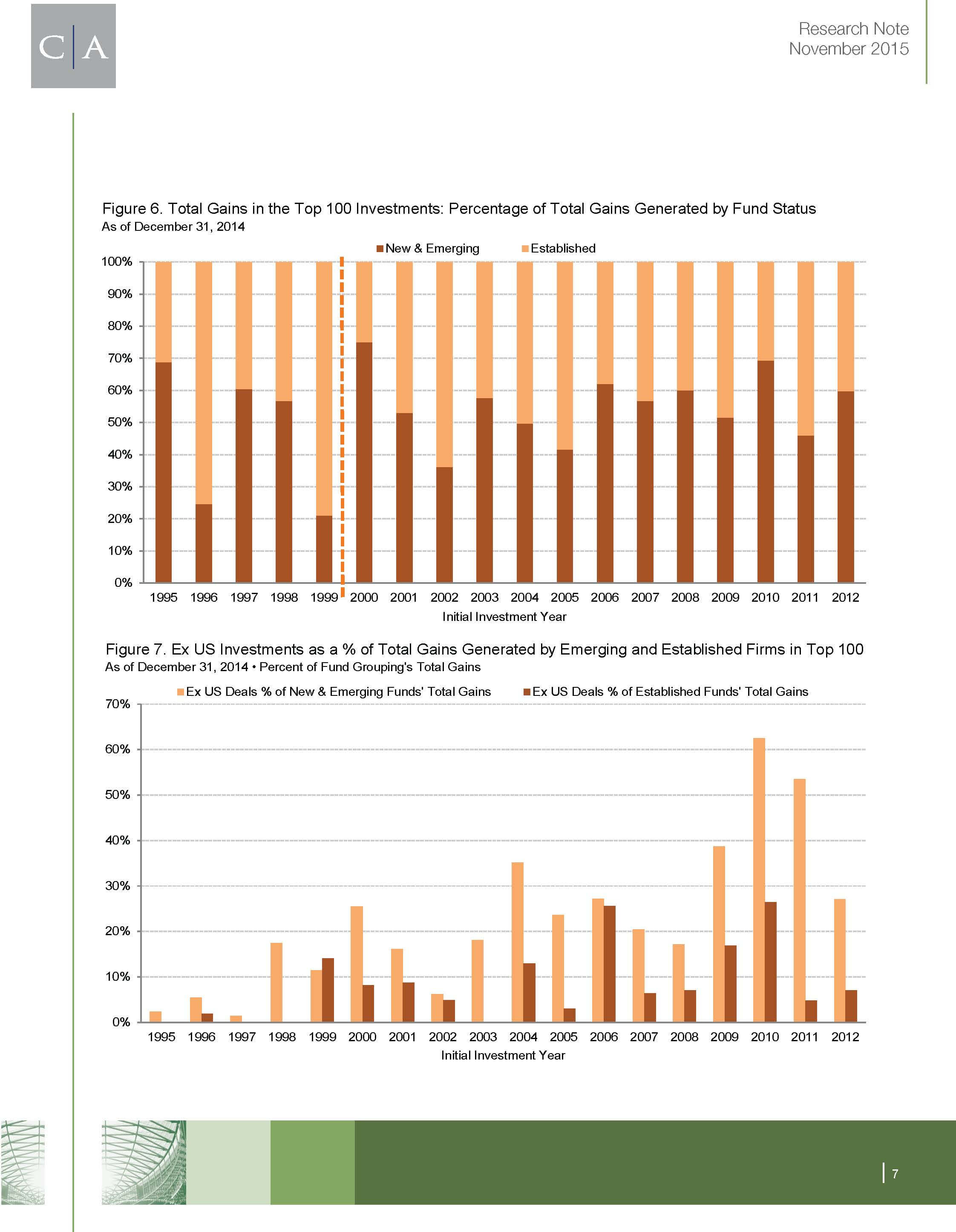

- the composition of the firms participating in this level of value creation has changed, with new and emerging firms consistently accounting for 40%–70% of the value creation in the top 100 over the past 10 years.

Value creation is becoming more broad based

Pre the dot-com and in a shake up period proceeding it there was a concentration in the top 100 deals. Looking at the period of 2007 to 2012, this has shifted.

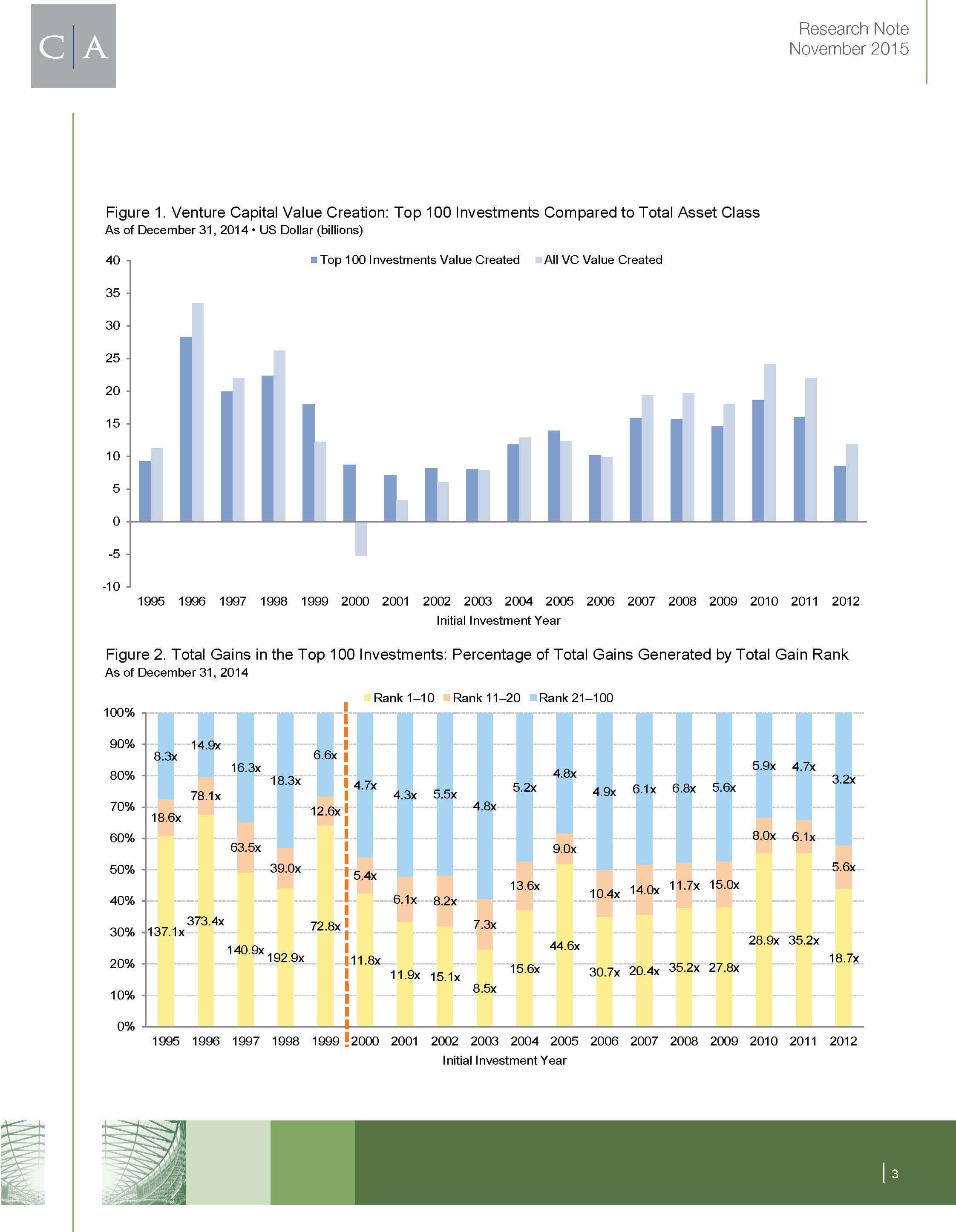

Figure 1. Venture Capital Value Creation: Top 100 Investments Compared to Total Asset Class As of December 31, 2014 • US Dollar (billions)

In the pre-2000 period, the top 10 investments accounted for an average of 57% of the total gains, ranging from 44% to 68%. Post-1999, the top 10 investments accounted for an average of 40% of the total gains generated by the top 100 investments per investment year (Figure 2). This is an almost 50% broadening outside of the top 10 hits.

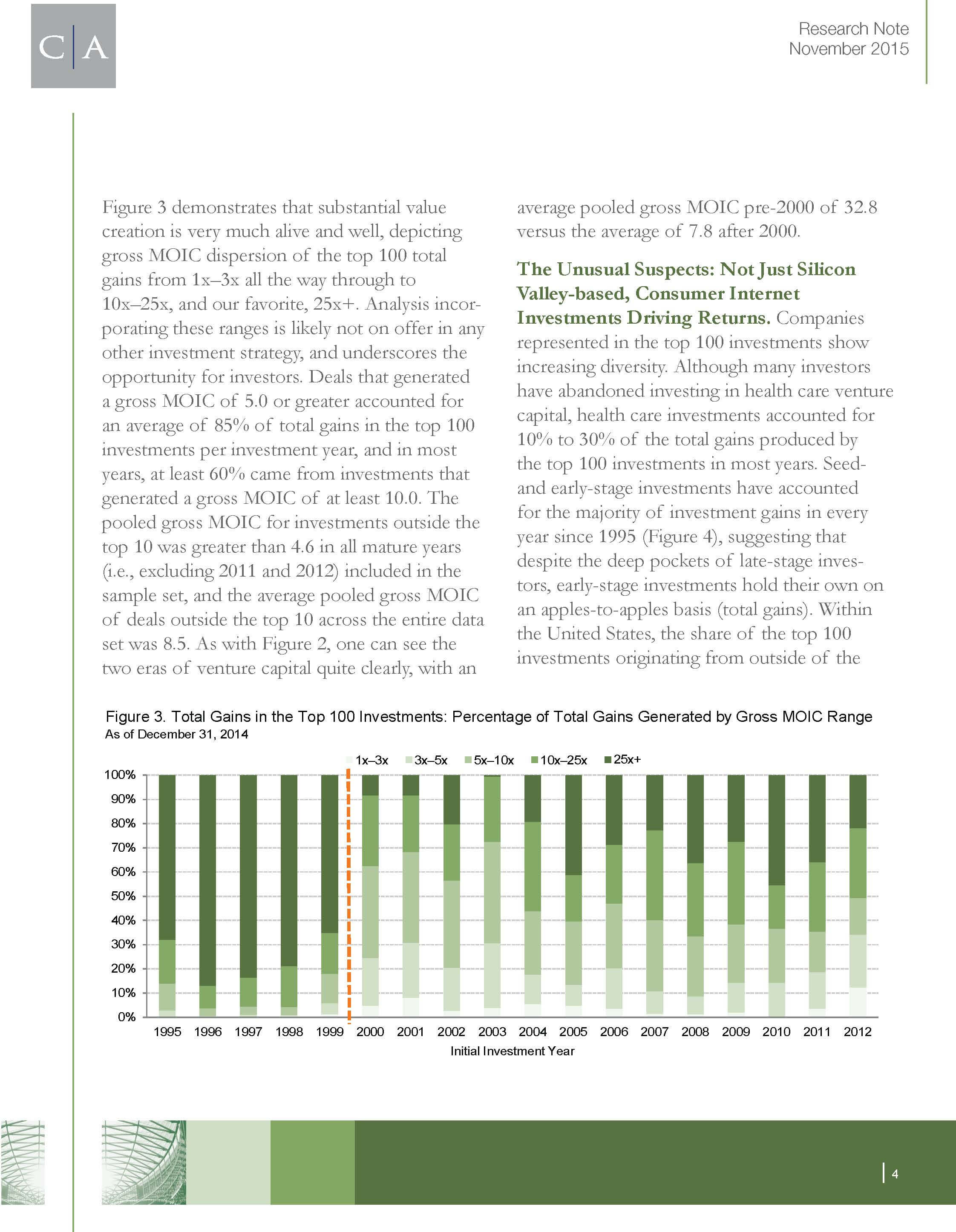

Whilst the pooled gross MOIC (Multiple on invested capital) generated by the cohorts has tumbled from the lofty highs of the comparable tech bubble cohorts (average pooled gross MOIC pre-2000 of 32.8 versus the average of 7.8 after 2000), returns are still strong. Deals that generated a gross MOIC of 5x or greater accounted for an average of 85% of total gains in the top 100, and in most years, at least 60% generated a gross MOIC of at least 10x.

Figure 2. Total Gains in the Top 100 Investments: Percentage of Total Gains Generated by Total Gain Rank As of December 31, 2014

So if you take together a total increase in all asset value creation (fig 1), less concentration of returns within the top 100 deals and robust MOIC multiples, there is an obvious case to be made that the concentration of successful funds isn’t holding up.

Where money is made is changing

The mix startups represented in the top 100 investments show increasing diversity.

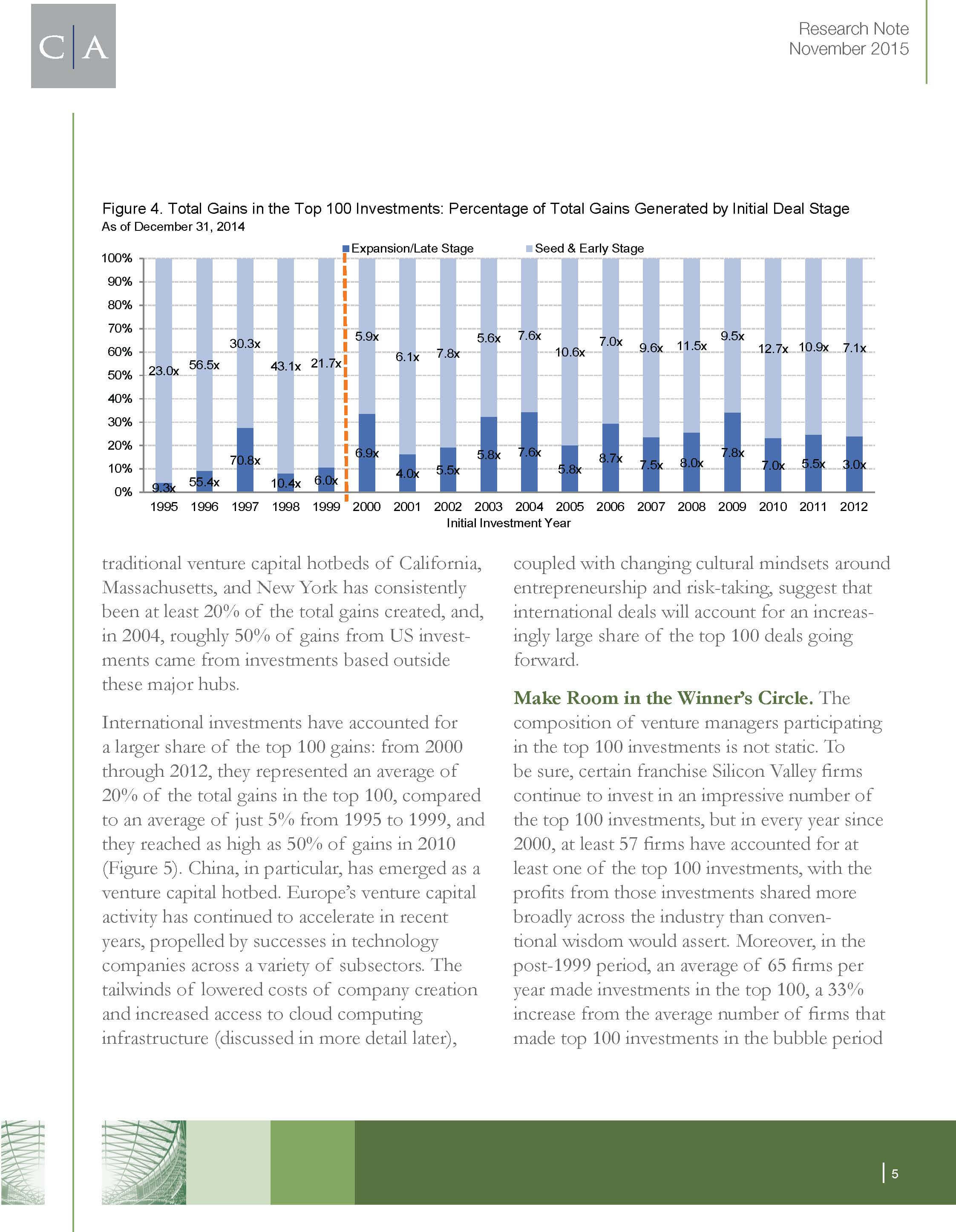

- Early stage returns rule supreme: Despite the deep pockets of late-stage investors, early-stage investments hold their own on an total gains basis. In fact seed and early-stage investments have accounted for the majority of investment gains in every year since 1995 (Figure 4). The rise of the micro VC comes to mind here.

Figure 4. Total Gains in the Top 100 Investments: Percentage of Total Gains Generated by Initial Deal Stage As of December 31, 2014

- Shift outside of US hubs: The stalwarts of California, Massachusetts, and New York have consistently been at least 20% of the total gains created, but in 2004, about 50% of gains from US investments came from outside these hubs.

- Returns from many sectors: Healthcare, a sector that has fallen out of favor still returns 10-30% in most years.

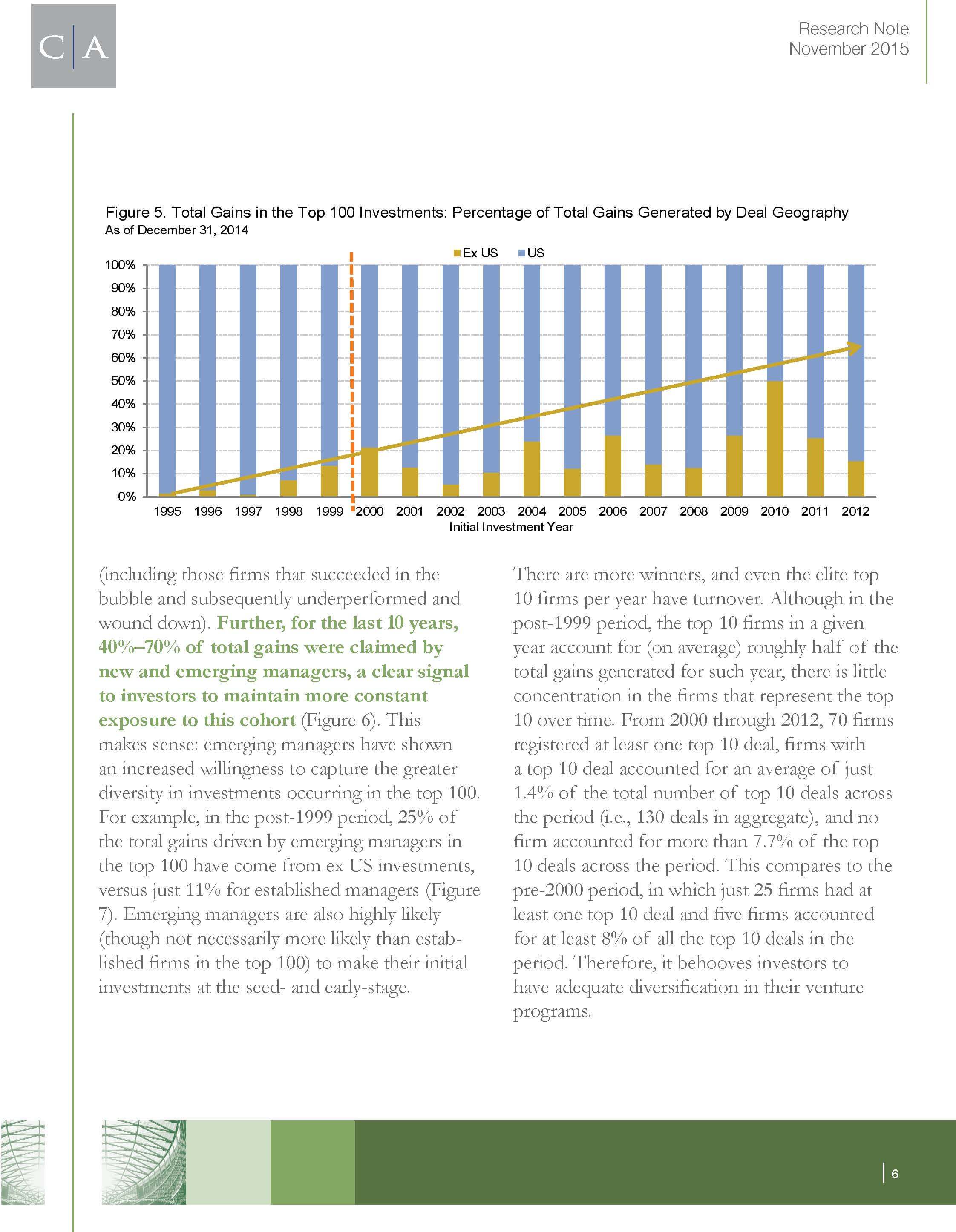

- International investments now contribute a larger share of the top 100 gains: From 2000 through 2012, they represented an average of 20%, compared to an average of just 5% from 1995 to 1999, with a high of 50% in 2010 (Figure 5). China is superhot and Europe has accelerated in recent years. This will only continue.

Figure 5. Total Gains in the Top 100 Investments: Percentage of Total Gains Generated by Deal Geography As of December 31, 2014

There is not as much consistency in top 10 firms as you would think

The composition of venture managers participating in the top 100 investments is not static:

- Top 10 firms perform, some of the time: Post-1999 period, the top 10 firms in any year account for roughly half of the total gains generated for such year, but there is little consistency as to whom that is over time.

- The top 10 deals are not just for the top 10 like they used to: Pre-2000 just 25 firms had at least one top 10 deal and five firms accounted for at least 8% of all the top 10 deals in the period. From 2000 through 2012 this shifted, 70 firms logged at least one top 10 deal, firms with a top 10 deal accounted for an average of just 1.4% of the total number of top 10 deals across the period (i.e., 130 deals in aggregate), and no firm accounted for more than 7.7% of the top 10 deals across the period.

- The top 100 deals are highly fragmented: Certain franchise Silicon Valley firms still rank in the top 100 investments, but in every year since 2000, at least 57 firms have accounted for at least one of the top 100 investments. Post-1999 period, an average of 65 firms per year made investments in the top 100, a 33% increase from the average number of firms that made the top 100 investments in the bubble period

- New/emerging funds claim more than established funds: For the last 10 years, 40%–70% of total gains went to new and emerging managers, a clear signal to LPs to consider this this cohort!

- Established funds are missing out outside the US: In the post-1999 period, 25% of the total gains driven by emerging managers in the top 100 have come from ex US investments, versus just 11% for established managers (Figure 7).

Figure 7. Ex US Investments as a % of Total Gains Generated by Emerging and Established Firms in Top 100 As of December 31, 2014 • Percent of Fund Grouping’s Total Gains

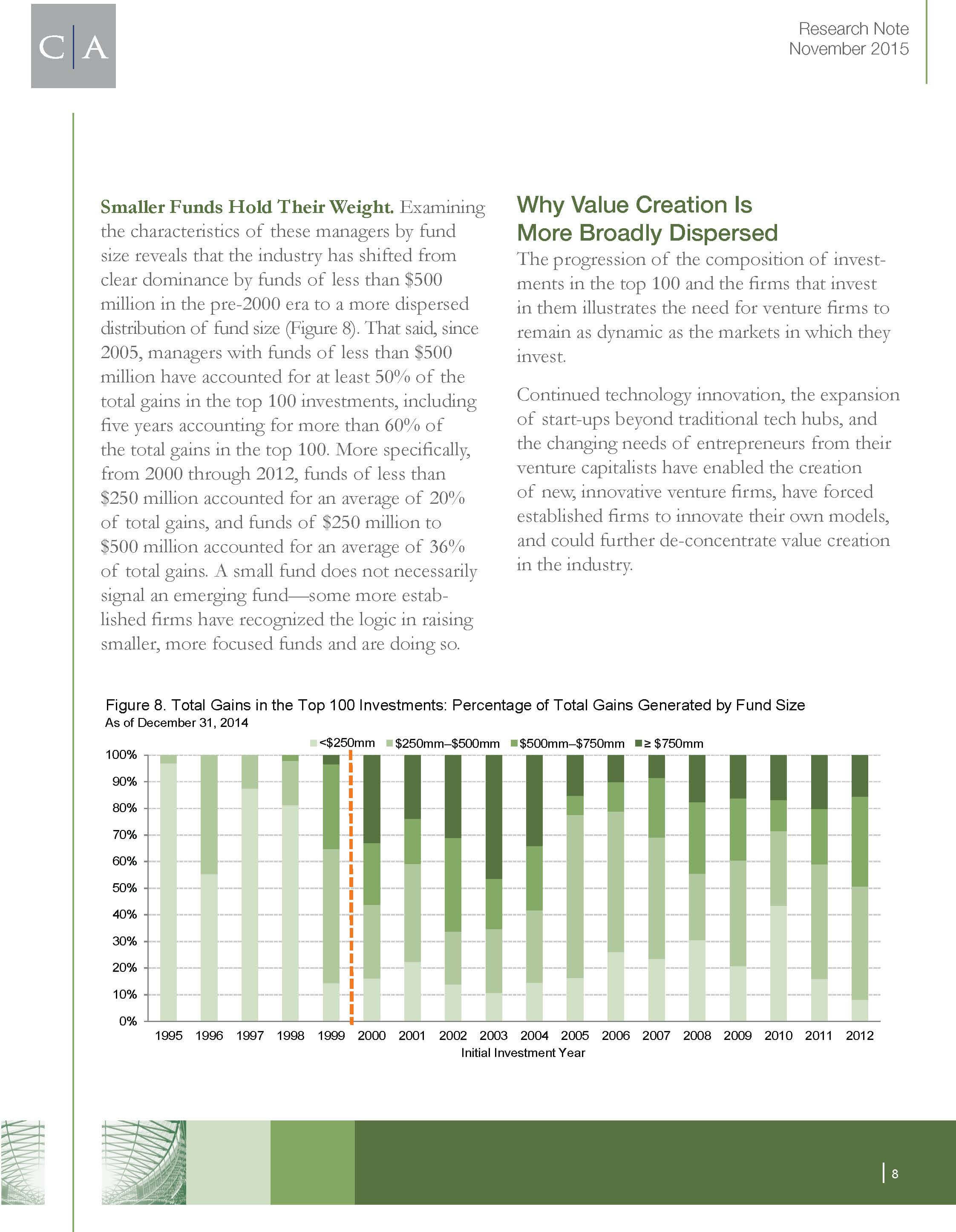

Why Value Creation Is More Broadly Dispersed

The changing composition of the top 100 performing companies and the technologies that enabled them, the funds that invest in them and the operating environment precipitate the need for firms to be more dynamic and innovate their own models. As returns come from new markets or just outside of traditional hubs and new, innovative venture firms come to address challenges, there may likely be further dilution in value creation in the industry.

Some of the changes occurring VCs need to adapt to are:

- Lean models: The declining costs of building technology companies have enabled technology entrepreneurship to expand beyond traditional venture capital hubs. Easily accessible, scalable, cloud-based computing capacity has obviated entrepreneurs’ need to invest substantial capital in infrastructure hardware, which has in turn led to high-quality companies being created in a wider range of geographies. US-based venture firms willing to invest in less trafficked US regions and abroad, as well as venture firms based internationally, have captured the value created by a broadening geographical opportunity set.

- Active support of portfolio: VCs are starting to reevaluate their roles beyond pure capital, with many focused on how they can improve the ways they add value to portfolio companies. VCs can no longer simply compete on capital alone; entrepreneurs today have options and venture capital is not the cottage industry it once was. See next point:

- Tech impacts scale and time to market: The pace of innovation continues to accelerate, and innovative startups are increasingly addressing global markets from the moment they begin selling products (e.g. cloud, mobile, gene sequencing). Given the explosive growth rates that these changes in technology have enabled, VCs have increasingly focused on how they can help their companies scale in an sustainable, efficient manner, particularly since commitments have become sizeable! One obvious example is the provision of Operating Partners (e.g. Open View and a16z).

- Willingness to start from scratch has increased: There are more second time founders and seasoned staff coming out of venture backed firms. In addition, there are increasingly more principals and partners going out on their own to carve out niches where they see opportunities. Part of these newer firms’ success relates to their networks with younger entrepreneurs; however, these venture firms also deserve credit for pioneering a new wave of specialization of venture capital. 10 years ago investors may have referred to a specialized VC as one focused only on technology, the emerging VCs succeeding today have refined their focus to certain subsectors (such as IT infrastructure and ecommerce) or thematically (transformational data assets). This focus enables new firms to compete and provide value add.

Conclusion

The data is by no means definitive, but there are starting to be some trends in the direction that innovation in venture capital has already happened and will only accelerate leading to further fragmentation of returns.

Outside the scope of this research report is the potential for new platforms to disrupt aspects of early stage investing, such as with AngelList and their syndicates (US for now) and crowd funding platforms which are gaining regulatory approval and increasing credibility (E.g. crowdcube in london which advertises deals on the Tube).

I personally believe one of the key points here is the combination of the ability of startups to scale with limited capital and gain traction in the early stages, and the rise of the micro-specialised-VCs that can arguably better support those companies and in doing so allocate capital in an efficient risk-adjusted basis and get solid, consistent returns.

No doubt the big boys like a16z (sort of a new fund compared to Bessemer), in some regards FRC (at early stage) and others hold real advantages over smaller funds, particularly the micro-vcs. The honest reality is bigger funds have more management fees and with these, if so inclined, you can run all sorts of initiatives to support and attract the best startups. Furthermore, with more dry powder and brand you can muscle your way into deals and getting more than your pro-rata at the expense of other smaller coinvestors (I know this for a fact to be true). But to some extent you are only as good as your last deal, so larger funds can rest on their laurels for only so long with their competitive advantage.

Btw, check out Cambridge Associates and their research here. They have some super stuff and in my experience, very smart and affable guys. This is a synopsis of their research and all the smart stuff is attributed to them!