Tl;dr: Understand convertible note terms like a pro! You can save half a million dollars of upside and significant downside by understanding how convertible notes are calculated at conversion. You can furthermore limit your downside by adding a few simple clauses to note agreements, these prevent convertible note holders getting excess liquidation preference rights, as well as bonus anti-dilution and dividend rights. This blog has a free excel template below and teaches you how conversion happens.

Download

“Raise a convertible dude, it’s easy and cheap” they say. Sure, that used to be true but with the advent of ‘series-seed’ documents in many countries, this is not

For experienced and savvy founders, they may with their attorneys purposefully draft convertible note documentation sparsely, leaving significant latitude for interpretation and negotiation with series-A investors. But this is very much for practiced hands, to whom I don’t believe many exist. Therefore, for the great unwashed 99% of us, you need to know to be in the know.

This blog seeks to raise awareness on two critical areas that both investors and founders are either not aware of, or otherwise do not understand, let alone can calculate. These are:

- The three manners conversion can happen for convertible note terms

- Phantom liquidation preferences, as well as anti-dilution and dividend rights

There is no model available which can calculate the conversion scenarios, so I have made a template with every meaningful variable I can think of. In this model, you can type in your assumptions and see the results as well as compare the outcomes.

Knowledge is power, but in this case it’s also money. Using the assumptions in this blog there is a 4.3% difference in shareholdings for founders between the Percentage-Ownership and Pre-Money method. That’s $428,571 on paper! If you’d like to save half a million, maybe you should read on?

The scenario setup for convertible note terms

Seed round

You raise a Convertible Note (“CN”) of $1m from some Angel Investors. The note has a discount rate of 30% and a cap of $8m. You try save money on the legal docs by using a template which is ambiguously worded. Doesn’t matter, the Series-A is when the details get sorted, right? By not doing a series-seed structure you also put off a negotiation on price. All the usual thinking. But fundamentally, your docs are ambiguously worded and the specifics of what actually happens when you do the fabled series-A is not clear. Will there be one or two pricing discussions? Find out later…

Series-A

After many sleepless nights you hustle to your next funding round, the series-A. You attract Khaki Capital to lead the round. They say they will invest $2m at an $8m pre-money valuation. You accept the term sheet and sign it. The lawyers get together and start doing DD. Everything goes well till they dig into the cap table and the convertible note…

Khaki Capital think they are going to own 20% of your startup once the round close. The Partner calls the Angels and they think with their math that they own 13% and have a liquidation preference of 1.4x. You’re confused and believe you will own 60% and have a 10% ESOP post money (Which is about 15% pre, you expected the option-pool shuffle), but didn’t agree to give the Angels liquidation preferences? That adds up to 103%. Clearly no one is on the same page here and doesn’t understand the ins and outs of convertible note terms. Something is clearly rotten.

No one knows the method upon which share prices for convertible notes will be calculated, and therefore what the post and pre money price per share is. Someone, if not everyone is going to be unhappy.

The key assumptions we will use in the model:

| Series-A Pre-Money Valuation | 8,000,000 |

| Series A Investment | 2,000,000 |

| Convertible note Principal Plus Accrued Interest | 1,000,000 |

| Discount Rate for Conversion of Notes | 30% |

| Cap for Convertible Notes | 7,000,000 |

| Shares Outstanding (Pre-Investment and pre ESOP) | 1,000,000 |

| ESOP | 10% |

Overview

The great thing about a priced round is you know how much you own. I’ve had famous investors pass on deals as they don’t do CNs.

I don’t do CNs. I want to know how much I own. – Nikesh Arora, President, SoftBank

CNs are not in fact as simple as you think, they’re messy and confusing, it’s just that TechCrunch etc doesn’t talk about this ‘boring stuff,’ or they do but you don’t read those posts, because they are actually boring.

As was disclosed in the start of this blog, depending on how you choose to do the math, you can end up with different shareholdings. Clearly, conversions are not created equal. The first rule of CN club is there is not one way to calculate conversion price per shares at the qualified financing. There are in fact three different methods to calculate the conversion in convertible note terms. Yes, three!

The painful thing about the ambiguity of the CN conversion is you are opening up a whole new pricing discussion. This debate happens toward the end of the process, not at the start, after which the S-A investors issued a term sheet where they set the value and the price per share. Everyone thought there was a defined price per share, but now there are three potential values which dictate their shareholding. This has the potential, when taken with other questions, to kill or significantly delay the deal closing, which is a big deal for founders who need the money to execute. Now everyone has to compromise and use their last ounce of negotiating leverage at the risk of souring the relationships.

We’re going to go through each of convertible note terms methods for conversion step by step including the math now. You need to know this stuff or it is going to cost you.

Basic Series-A math to calculate valuations and price per share

Calculations without CNs are simple. Khaki Capital invests $2m at a $8m pre. You add the two and the post is $10m. The shareholding of your S-A investor is, therefore, the $2m investment divided by the post valuation of $10m, which is 20%. Simple, right?

Now to calculate the per share value, you take the pre-money valuation which is $8m and divide by the shares outstanding:

- No ESOP: If there was no ESOP, this is simply $8m over the 1m shares outstanding so $8 per share

- ESOP: You need to issue shares before the deal so the outstanding shares increase by 142,857 shares (the ESOP shares are 12.5%). This means we have 1,142,857 shares. So the price per shares is $8m over 1.142m, which is $7

In this example and in the examples we will go through, we assume that the ESOP pool of 10% that VCs ask for always comes out of the pre, not the post-money! This is pretty standard practice. So regardless of the size of the ESOP the founders stomach the whole lot.

So, if the founders own 100% pre the A-round, they will end not with a dilution of 20% but 30%. They own 70% after the A-round and new ESOP (I assume there is no ESOP before to make the math focused on the issues we want to learn about). Understand that the ESOP is made pre the deal, so post the deal there is a 10% pool. Assuming 20% dilution at the A the ESOP is 12.5%, which itself gets diluted to the 10% post.

Hopefully this gives you a grounding before we dig into the conversion math. The math gets a lot more complicated from here due to the conversion math of the CNs. If you don’t understand the basics, watch this video and read this blog to get another free template to learn with:

Three methods to calculate conversion

The key thing to understand is that the CNs convert and their shareholding comes out of the founders’ or the VC’s stake, or limits the stake of the Angels, but always adds up to 100%. The method decides how much from whom.

At a high level, this means the founders post ESOP will own less than their expected 70% or the VCs will own less than the 20% they think they are getting. Percentages are not the best way to think about the math of these mechanics though. It’s better to think in terms of the effect on pre and post money, or it’s derivative, the price per share.

Note that decreases in the pre are bad for founders and increases in the post are good.

So, translated into our lingua franca, the base line for ‘who is unhappy’ is the pre of $8m. If the pre decreases, the S-A and CNs get a larger shareholding at the expense of the founders. So, for the conversion of CNs, if the pre doesn’t go down below $8m the A investors will have less than their 20%. Decreases in the pre means the price per share also go down so you understand the dynamic.

Let’s skip ahead now to the three methods and this will make more sense as we visualize it.

The three methods are as follows:

- Pre-money method: The pre is set at $8m. Best for founders and worst for S-A. As we just discussed this means the holding is coming out of the S-A and CN share. This is seen by the post increasing to $11.43m from the simple math of $10m

- Fixed percentage method: Worst for founders. Likely what VCs expect. The pre decreases the most to $6.57m. The post is $10m. This could be called the post-money method

- Dollars invested method: The balanced method. The post is $11m and the pre is $7.57m. You can see the pre and post are both higher than the previous method, but less than the first one

Below is a pretty summary of the methods:

Comparison of outcomes

Following the summary of the methods of convertible note terms we just discussed, here is a summary of the outcomes for the three methods so you can see the effects numerically. You can see the effect on the ownership and the valuation.

Introduction to the convertible note terms model

At the top of the model for each sheet calculating the mechanics we have the Assumptions. These can be changed in each sheet. To properly compare the outcomes across the three you need to set them the same though (obviously).

The only thing that is different in each of the assumption sheets is the calculation of the post money valuation. If you want to see that, check for it in this section. Otherwise, the sheets are purposefully set up to look consistent.

If you want to change the numbers for your specific circumstance, then only type in the yellow boxes with blue text. These are the pre, investment from S-A, the CN numbers (Principal, discount, cap), shares outstanding and ESOP size. The CN overhang switch and liquidation preference multiple are used to illustrate the liquidation preference overhang, we will discuss at the end of this blog on convertible note terms.

Note, to keep things simple, I assume the CN totals a million $, so includes interest. If you have interest, which is generally legally required (In the USA, approx. 5-7%), put in the total, not just the principal.

The ‘Discount or cap’ section calculates which one will be used. In this example, it is always the discount as it is more favorable to the Angels (It won’t be if you change the assumptions).

The ‘pre money calculation’ calculates the pre. The only number that changes is the post-money. If it is higher, then the pre is higher and vice versa. The deduction of the ESOP is to illustrate the ‘effective ‘pre-money.’ Since founders need to include an ESOP prior to the investment, the effective pre is lower. This is a topic under the ‘option pool shuffle.’

The ‘price per share’ section calculates the price per share (surprise!). Firstly there is the S-A price. You will notice this is not $8 per share as the number of shares have increased due the ESOP. Therefore S-A price per share looks very similar to the effective pre in the pre-money calculation section! The price for convertibles in both discount and cap scenarios are shown, but only one is used. This is the discount in this scenario. The cap would have to be a lot lower to have a lower price per share to be used by the CNs.

The ‘ESOP’ section illustrates the impact of issuing an ESOP out of the pre, not post money. It’s 1.4x the size! Owsies.

The ‘Convertible note liquidation preference overhang’ is used to illustrate the overhang effect we will discuss later. Let’s skip it for now.

In the ‘Stockholders’ section, you can see the ownership per shareholder in the pre and post investment state. There is only one line item for the CNs. The model automatically uses the discount or cap as required.

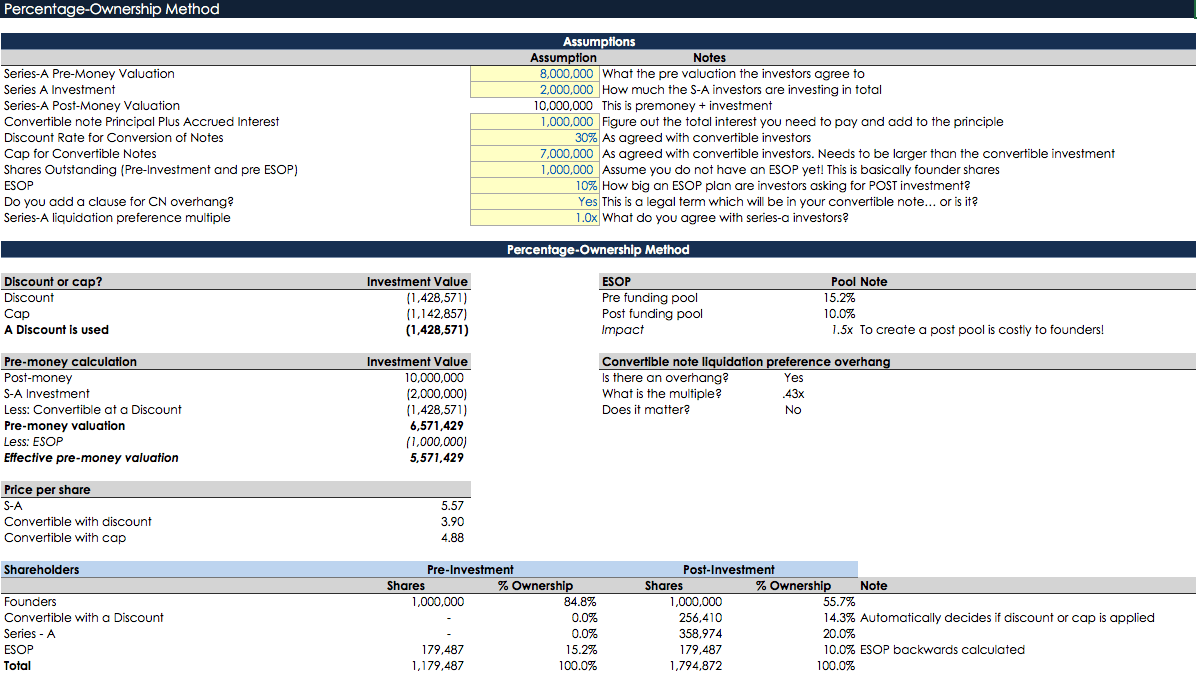

Method 1: Pre-money method

The pre-money method is best for founders as was discussed. Founders end up with 60%. Note in all cases the number of shares they own always remains constant at 1m shares. To grant equity to others they issue new shares which is how they get diluted.

At the top of the sheet, you can see the post money is $11.43m. This is the highest number of all three cases which means it’s good for founders and bad for everyone else. Have you ever heard an angel or VC say, ‘yeah, let’s go with a higher valuation!” Yeah, neither have I. That’s because their ownership is calculated off the post, so a lower post is good for them. VC’s obviously don’t like this method since they own less than they thought. The way smarter VCs deal with it is writing a term sheet which explicitly states the post they are investing in and the pre therefore adjusts accordingly, making the issue the founders to deal with.

The S-A investors’ share price is $6.86 which is calculated by dividing the pre-money of $8m over the numbers of shares outstanding (1.17m shares). The shares are the sum the founders have plus the ESOP shares needed to get to a 10% holding post-investment. This results in them holding 17.5%.

The pre-money is $8m and the effective pre is $6.86m. The pre is also the highest in all three cases as mathematically makes sense. Since the post is higher, after making deductions of the S-A investment and the CN at a discount, the pre results in a higher result. The same deductions are made in all three cases, so what matters is the starting point of a higher post.

The post is the highest as it includes the total value of the notes. The percentage-ownership does not add this at all, and the dollars-invested does, but not the conversion value (just the principal and interest amount).

So, the two defining points about this method are:

- The pre is set and the price per shares is calculated on that. This is $8m pre which is what we did in the simple S-A math, but the post is higher

- The post is the highest as it includes all the investments at their conversion value

Let’s get into calculating the value of the convertible notes. There is both a cap and a discount. In effect, only one is used as a liquidation preference. You don’t get to use both. In this case, the discount is the ones used. Why? Let’s do the math.

The discount is calculated by deducting 30% from the price per share the S-A investors use. So (1-30%) of $6.86 is $4.8. The conversion value is $1.43m. Our cap has a conversion value of $1.143 which is lower. Obviously, if you are an angel you want your investment to be worth more, right? So, which value would you pick- the higher conversion value and the lower price per share.

In this method, the founders and S-A investors are diluted in proportion to their shareholding. So, the S-A investors thought they were getting 20% but they are getting diluted the % holding of the CNs which is 12.5% so they own 17.5% now (Which is 2.5% less). The ESOP is fixed so the founders who have 70%, take the 10% of the ESOP too, which is therefore 80%. The founders take the other 80% of the dilution which is 10%.

According to Cooley, this is the most common method used in convertible note terms.

Method 2: Percentage ownership method

This is the doomsday scenario for founders. They take a hammering on the full value of the CN and the VC is shielded from it entirely. The pre-money is $6.57m and the post is $10m. The founders end up with 55.7%.

The VC is happy and gets the shareholding they thought they were getting: 20%. Under this method, the post-money which their shareholding is based on is fixed at $10m.

The CNs are ecstatic as they get the highest shareholding in this case which is 14.3%. Why is this higher than in the pre-money method? Well, their price per share is based on a discount to the price per share the S-A invest at which is $5.57. A 30% discount is $3.9. Since the pre-money is less so is the price per share. Bad news for the founders.

Again, we don’t use a cap since the price per share under that scenario is $4.88 which is 1.25x higher (more expensive) than the discount approach.

It is interesting to note that the pre ESOP is the largest too in this case. The ESOP you need to make to compensate for dilution post investment is 15.2%, which again comes out of the founders’ shares.

So, the two defining points about this method are:

- The pre is the lowest and all the cost comes out of the founders (lower pre is bad for founders)

- The post is set and the price per shares is calculated on that. None of the investment value is included in the post valuation like it is in the other two cases

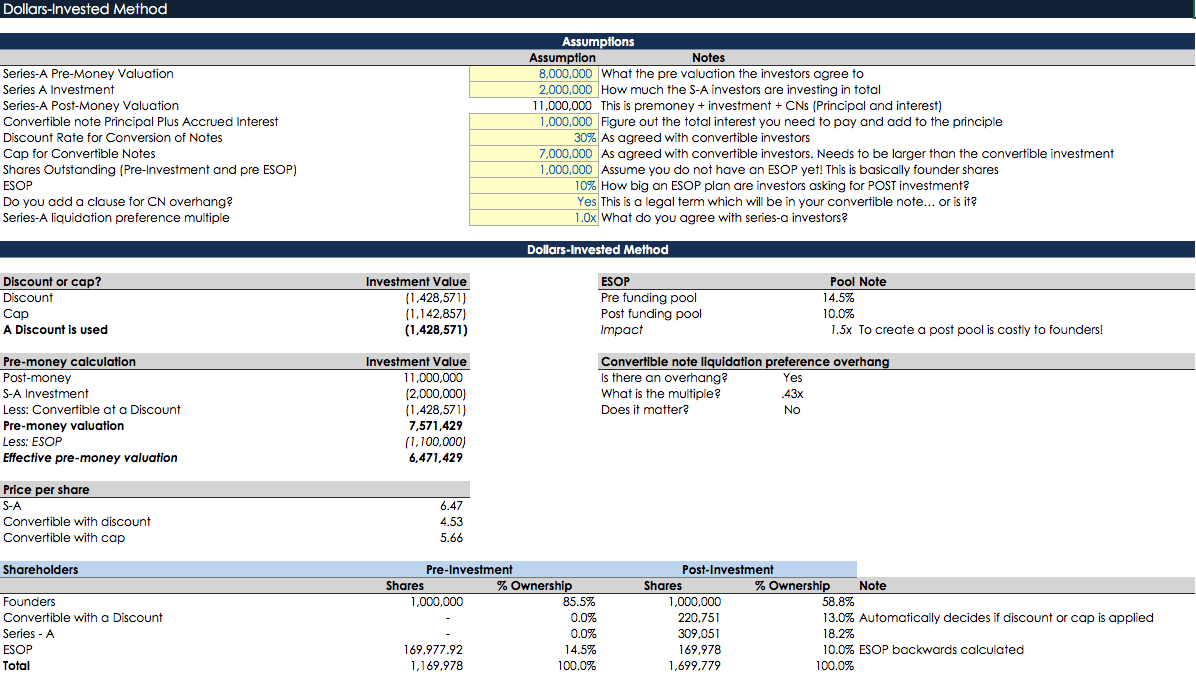

Method 3: Dollars invested method

This method is less likely to be chosen as the default since it isn’t obviously beneficial to either party. It is likely to arise from a ‘freak out’ by founders on being told to use the percentage-ownership method just discussed. This is, therefore, the one parties settle on depending on the leverage founders have. According to Cooley:

“Unless it is expressly indicated in the term sheet, many entrepreneurs consider using this method to be a material deviation from the agreed upon term sheet and object to its use.”

In this method, the post is calculated similarly to the pre-money method. It gets larger by adding the principal (and interest) rather than the conversion value. So, the post is $11m. The consequence of this is the pre is $7.51, a million higher than in the percentage-ownership method. We add the pre, the S-a investment and the CN base value; in the previous method, there was no addition of the CNs.

The founders own 58.8%. It’s worth noting that’s what happening in this method is the founders are getting all the dilution of the difference between the conversion value of the CNs ($1.43m) LESS the principal and interest ($1m) which is $0.43m. The principal and interest are added to the post so the Swit-A investors only take dilution on that portion. In effect, the founders treat the principal and interest as being a new investment and only get diluted by the CN upside from the discount (or cap). The rationale according to Cooley is:

“converting debt into equity without a discount does not change the Series A Investors’ percentage ownership of the enterprise value of the company,

so they are still getting the deal for which they bargained.”

The S-A investors own 18.2% and their price per share is $6.47. This is not as positive as the percentage-ownership method but a lot better than the pre-money method. They are a lot closer to the 20% they thought they would get.

Again, the discount is used by the CNs as the price per share is $4.53 and the cap is $5.66. To the benefit of the founders, the CN price per share is higher, as is the S-A. The ESOP size post investment is close to the pre-money method of 14.5% (vs 14.3%).

So, the two defining points about this method are:

- The pre is the middle valuation of the three. The founders take the dilution on the difference of the CN conversion value less the principal and then all the cost on the principal comes out of both the founders and VC’s pocket in proportion to their post shareholding

- The post is set to include the base value of the CN investment (principal plus interest, not the conversion value) and the price per shares is calculated on that

Conclusion to conversion mechanics

Congrats. You are now in the know. Download the model and have a look at it. It’s really simple if you understand what is added to the post money (or not). Now let’s talk about the ‘phantom’ stuff I briefly alluded to!

Phantom liquidation preferences or liquidation preference overhang

Did you know that convertible note terms are structured to give CNs more liquidations preference then they have paid for? This means you as a founder are literally giving money away in certain scenarios? And now S-A rounds are extending out, being infilled with more angel and seed rounds (high-resolution financing) which may use CNs AND the CNs are actually converting, the issue is all the more important to be aware of. No standard has been adopted to fix this, so you are going to be aware of it and fix it yourself. So let’s start off with what a liquidation preference is first.

A liquidation preference gives investors the option to get their money back, or to convert their preference shares into common and effectively liquidate their holding. These preferences have value. Founders and staff do not get any pay back until the liquidation is paid, which is bad if you don’t sell for as much as you were planning on (the norm)?

A 1x liquidation preference at series-A is pretty much standard in the current market. Now, since we are talking about convertible notes (let’s say Angel investors), in most circumstances your Angels convert their convertible notes at the same terms as the S-A; well most of the same terms that the S-A investors get (maybe not the same information rights, board seat etc, depending what you agree). This implies your Angels when they convert are getting the same economic terms which means a 1x liquidation preference. Well 1x you would think… The math may not work that way if you do not add an important clause into your note agreements!

That clause states that Angels in the CN only get a 1x liquidation for the value of their investment. Huh? If Angels invest $1m then they should get a $1m (1x) liquidation preference if that’s what you (think you) agreed to. May not be the case my friend! They may get a multiple liquidation preferences due to how math works.

Convertible notes have two key economic terms which are a:

- Discount: a 30% discount to the price per share the S-A get

- Cap: A max price per share they pay, in this model the cap is $8m which is not used

Most notes these days, with smart angels, always have a cap, though some hot deals can get away without a cap. Where there is a cap, there is the potential for the Angels to get a large multiple liquidation preferences where the pre-money valuation is a big multiple of the cap. The same thing applies to the discount, but where there is a big valuation increase, it’s far smaller than the effect of the cap (Use the model and type in the pre-money to $50m. The cap is 5x the value of the discount.) This is not good for founders and may also annoy your series-A investors as it can impact future round of financing.

A ‘phantom liquidation preference’ or ‘liquidation overhang’ is when your Angels get a liquidation preference greater than that your S-A investors negotiate (which is typically one times). In our model, it is an additional 0.43x. The other thing to note, is the CNs also get 0.43x more shares which they can vote with.

The model

Let’s go through the ‘Convertible note liquidation preference overhang’ section in the model.

There are three parts:

- The first tells you if there is an overhang or not. There is pretty much always an overhang.

- The second part tells you how large it is. In this case it is 0.43x. It’s important to understand it’s 0.43x over the principal. In your calculation, you need to deduct the principal, so it is not 1.43x. This is meant to show the additional preference over the base preference. In the assumptions section there is a toggle for the multiple the S-A investors have. So if the S-A negotiate for a 2x multiple, the CNs get an overhang of 0.86x!

- The third part tells you if the overhang matters or not, meaning are you impacted? The simple answer is to have negotiated a clause in your contracts so you toggle the assumption section for “Do you add a clause for CN overhang?” If it is “Yes” then this whole section doesn’t matter, but you probably didn’t think about this. did you?

So what does this really mean? Let’s play with the dollars invested method.

The Angels invested $1m and are getting a preference worth $1.43m. As we noted this is $430k more than they should. So, let’s say you sell for $5m. You own 58.8% but you don’t get 58.8% x $5m which is $2.9m. The CNs own 13% which times by $5m is $909k. This is less than their larger preference of $1.43 so they take their preference of $1.43m. The same math applies to the S-A so they take the preference too. That means they in aggregate take $3.43m, meaning $1.57m is left for the founders and ESOP. If the CNs didn’t have the overhang preference there is another $430k, so founders and ESOP get $2m to share. That’s not a bad days work if you nipped that overhang in the bud.

But what if the S-A valuation was $50m? The overhang from the CNs is 6.14x! Their preference is worth $7.14m. Between those two preferences, you get zerooooo. Zilch. Seeing why this is important now? The difference in size between rounds has a massive effect on the importance of this clause, so if you are high growth, you better deal with this.

This lawyer has a great write up to explain this more, or at least from a different angle.

What do I do if I didn’t think about this?

You end up with an awkward cap table. Later stage investors don’t like different and complicated, they like things simple. There are only three options now:

- You go to Angels and ask them to give up their rights: Clearly, this is not going down well at the next keg mixer, right? Why should they give up something of value?

- You stomach them: That’s life

- You get your investors to pull their weight: Your S-A investor can say they won’t fund you unless the Angels accept to wave their rights. This is unlikely to happen as it’s not really a deal killer

How do I avoid this situation?

It’s very simple, you just need to add a simple clause to your convertible note terms before they are signed! The steps are this:

- Get a VC focused lawyer who understands this witch-craft

- They either are aware of this already, or you ask them to include it since you know

- They add the term. Most angels won’t understand it, or will likely think it is reasonable anyway

What is the clause to add?

So you are aware, a lawyer in the US has shared a clause you can use. Share it with your lawyer. This declares what the preference, anti-dilution and dividend rights are but not the method they will be structured, which you can also do to make things more clear:

“Financing Conversion Securities” means securities with identical rights, privileges, preferences and restrictions as the Qualified Financing Securities issued to new investors in a Qualified Financing, other than (A) the per share liquidation preference, which will be equal to (i) the Note Conversion Price at which this Note is converted, multiplied by (ii) any liquidation preference multiple granted to the Qualified Financing Securities (i.e., 1X, 2X, etc. of the purchase price), (B) the conversion price for purposes of price-based anti-dilution protection, which will equal the Note Conversion Price, and (C) the basis for any dividend rights, which will be based on the Note Conversion Price.”

How is this legally structured?

Assuming this issue has been taken head on there are two ways lawyers will structure your cap table and shareholding. They both have tradeoffs. To simplify dramatically:

Option 1: Create common stock

- CNs get a combination of S-A shares and common shares. So 1x the value in common and 0.43x in the S-A in the model example

- The downside is they have 0.43x shares which they can vote with. Since classes of shares vote this isn’t necessarily an issue unless your investors end up owning enough to veto you

Option 2: Sub-series of preferred stock

- This is the better option and increasingly common I am told. Cooley have it in their form convertible note terms

- Lawyers create a sub-series of stock (e.g. S-A-1) which is the same as the S-A stock except for the liquidation preference, basis for anti-dilution and dividend rights. The S-A liquidation price per share is different to the sub series

- The downside is the legal docs and cap table are more complicated. This means potentially more cost and some explaining in future fundraises

Conclusion to phantoms in your convertibles

Deal with this issue proactively. Just make it clear in your notes by adding a paragraph and you just don’t have this issue. When it comes to conversion, get your lawyers to apply option 2 and you have no issues with voting rights. It basically costs you nothing to do this.

Conclusion

I hope this has opened up your eyes to some of the hidden challenges in notes, some convertible note terms you weren’t aware of, and now you won’t face these financial constraints.

Download the model now and have a play. I can tell you that you can only internalize it by actually playing with the numbers. Trust me. It was not easy making this model look easy!

Thanks

Much thanks to Derek Colla at Cooley for the inspiration for this article and support. Special thanks to Hayden Smith at Cooley for feedback on the model.