Tl;dr: Eghosa Omoigui at EchoVC spent 9 months chasing Reid Hoffman to invest in LinkedIn around their Series-C around 2007. He was ultimately unsuccessful, but he leaves some learnings for us. He shared investment analysis for others to benefit. Read to understand how a venture capital investor thinks about investing in a company and how they communicate it to their partners and potentially their limited partners. And learn no matter how hard you hustle, sometimes things don’t work out.

About the VC investment memo

Eghosa Omoigui wrote the VC investment memo on LinkedIn. He was inspired by Reid Hoffman sharing his pitch deck and then David Sze from Greylock writing a short post on his thinking behind recommending LinkedIn to his Greylock partnership.

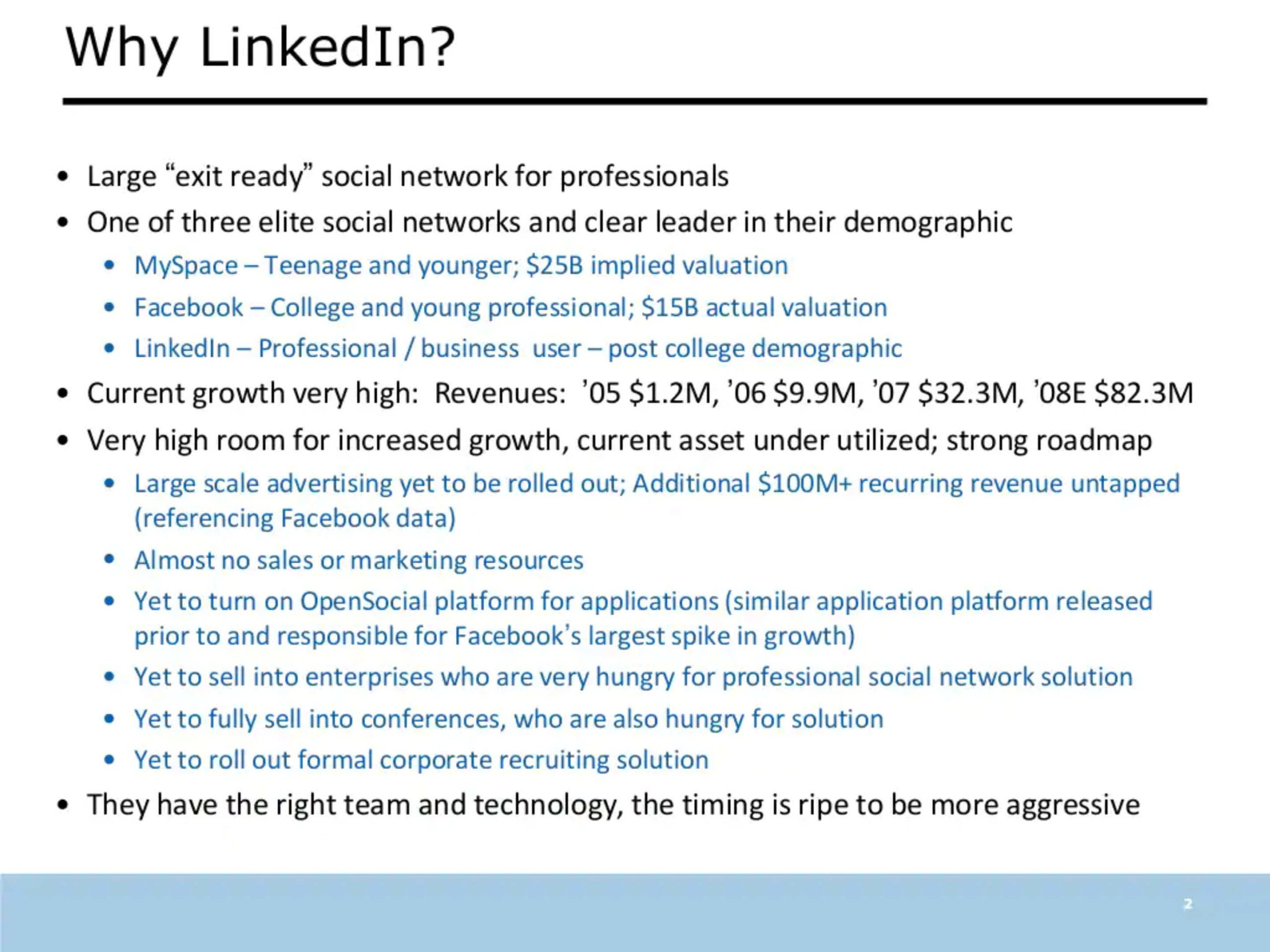

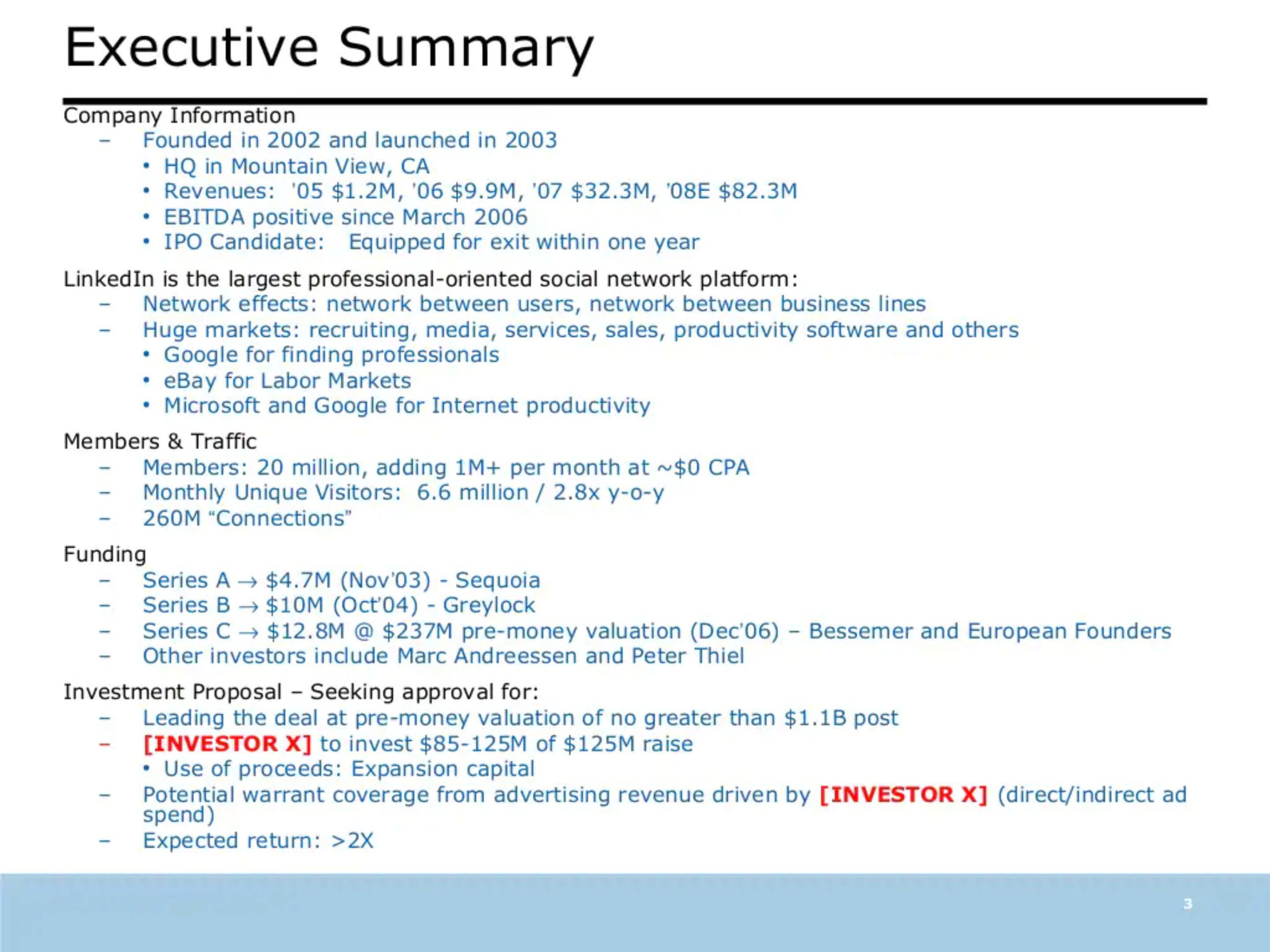

- See the Linkedin pitch deck.

- Read David Sze’s notes on his investment thesis.

After reading David’s post, he “jokingly offered to share my investment recommendation“. Fortunately, Reid and David were supportive and I was able to dig this out to share with you.

Eghosa’s story on the LinkedIN VC investment memo

This is my [short] story.

I actually don’t remember when I first met Reid Hoffman.

But I can never forget that day in early 2008 when my Blackberry phone rang and it was Reid on the other end. I had to step out of the staff meeting I was in to take the call.

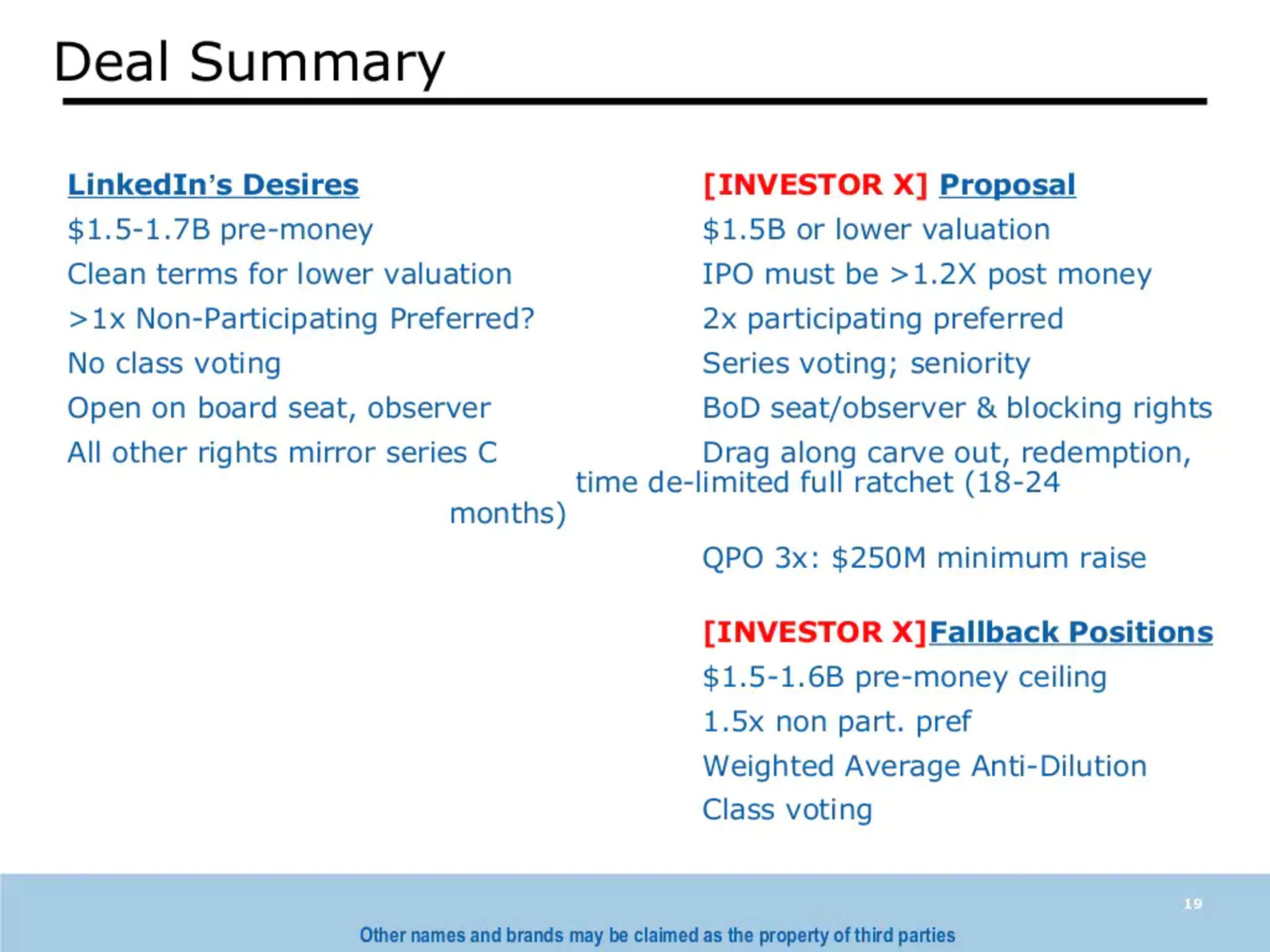

“Hi Eghosa. I just wanted to let you know we just got out of a board meeting. We will move forward with a financing round and you are my first choice. To be fully transparent, there are a few folks that aren’t fully on board because of some bad experiences with your firm in the past. But you have been dogged and I think you will be a great addition to our investor base. We don’t plan to optimize for valuation. All I ask is that you be fair and come with clean terms.”

In the midst of the current angst-filled chatter about unicorns (prime, subprime), unicorpses, decacorns etc., with the backdrop of the impending doom of a burst bubble and the subsequent wholesale destruction of unanchored dreams and undisciplined spending, I thought it would be useful to share my investment recommendation for a high-profile member of the last generation of unicorns (or high-octane companies as they were then known).

The background to this is part fun, heartache, knowledge, persistence, and (all) conviction. This timeline would span experiences that ranged from the 9 months I spent actively chasing after Reid:

- the memory of the look on his face when he realized I was serious about investing but only if he would reopen his Series C round (I was sorta kidding, Reid),

- the weekly emails I would send him reminding him of my interest in investing, his monthly replies which I didn’t consider to be rejections but more of a continuing conversation,

- the numerous visits to LinkedIn HQ after hours to talk about technology, people, impact and everything BUT LinkedIn,

- his oh-so-quiet recommendation to Peter Thiel and Mark Zuckerberg that I was worthy of consideration as a potential investor in Facebook,

- Reid’s thawing to the idea of a new round of financing, his agreement to meet with the investment committee in December 2007,

- my freaking out when I realized I would have to coordinate the meeting from Benin, Nigeria where I had to be for my sister’s wedding, the (until now undisclosed) fact that I was finalizing my divorce the same month,

- the behind-the-scenes drama with Sequoia wherein I learned they were dead set against my investing because my firm had antagonized them in 1999 and they hadn’t forgotten,

- the response I heard Reid gave them, viz “it’s eghosa that is investing, not his firm,”

- to the utter disappointment, I felt when I couldn’t get the investment done because the investment committee decided to play defense.

I was heartbroken, not just because of all the work and effort that had gone into the process, but also because I truly felt I had failed the entrepreneur and the company. Honestly, it still grinds.

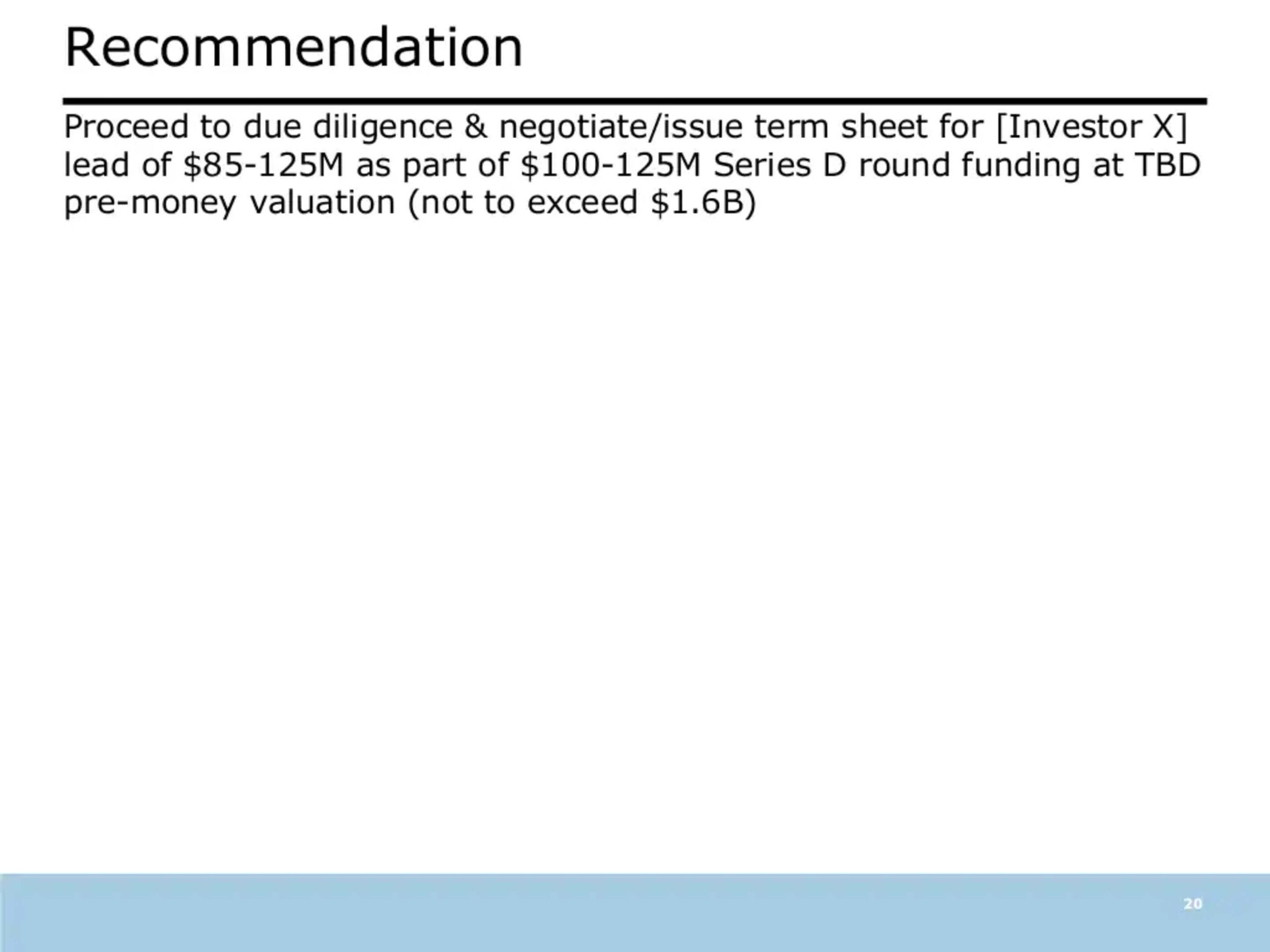

[Aside, Echose wrote in another blog:]“I left Intel Capital to start my own fund, partially frustrated by my seeming inability to communicate my conviction about paradigm-shifting companies like Facebook and LinkedIn sufficiently hard enough to be authorized to make large VC investments in them, and partially fueled by my desire to create a new type of venture fund, and a conviction that I would create a platform with the decision-making power to to do both. I was reminded by an ex-colleague a couple days ago about the upside of conviction when LinkedIn hit a $26B market cap, which achievement would have generated a 25x cash on cash return, in 5 years, on my initial $125M investment recommendation. It’s almost impossible not to curl up in the corner and weep when i think of the cost of conviction associated with my investment recommendations for Facebook I (9/07) or Facebook II (1/09).”

Anyway, I hope that this document is dissected from the POV of when it was done in 2008 and that those that are currently doing unicorn or logo-acquisition deals will also choose to share their analyses as I feel the investor ecosystem will benefit significantly.

Enjoy.

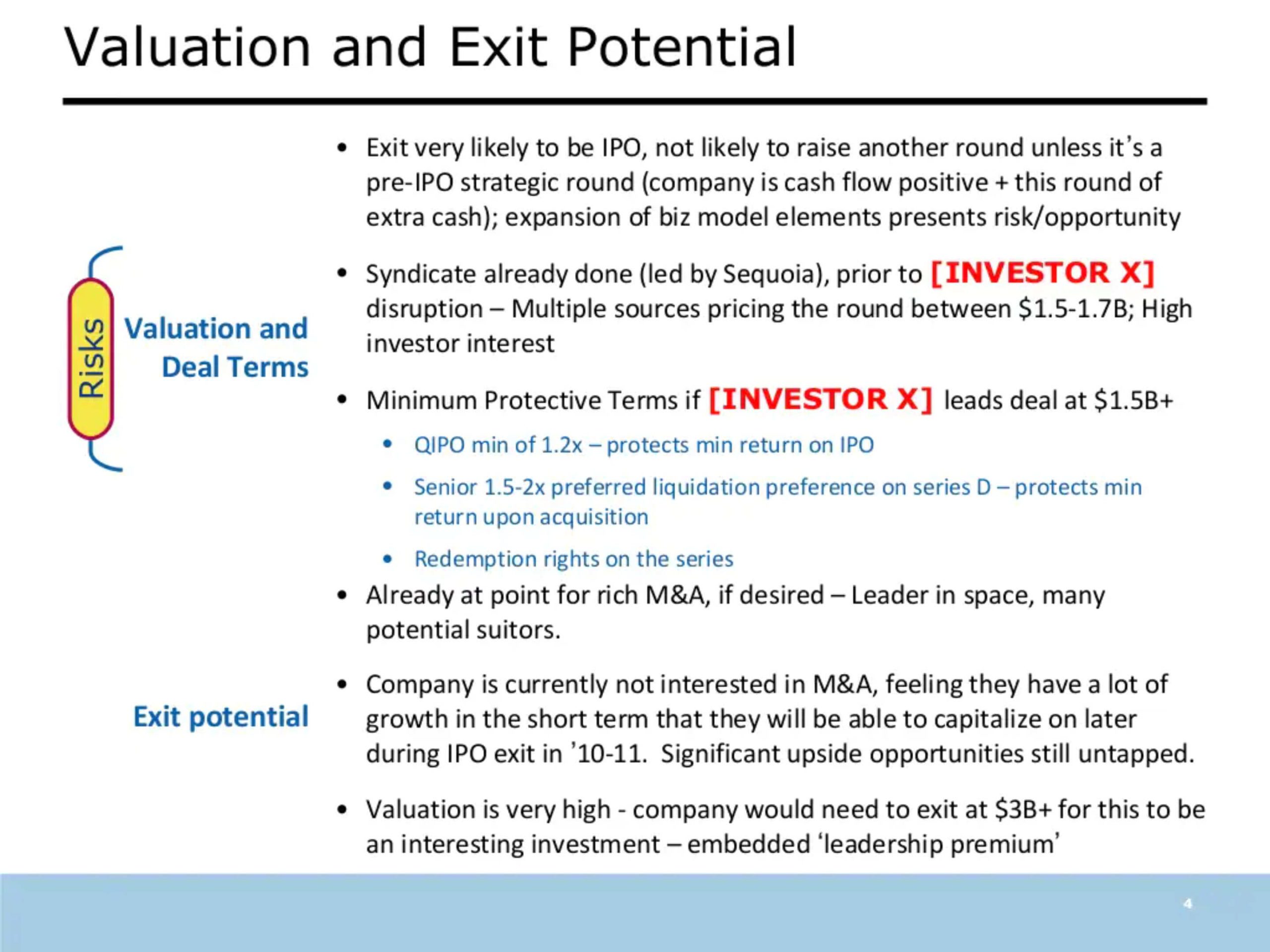

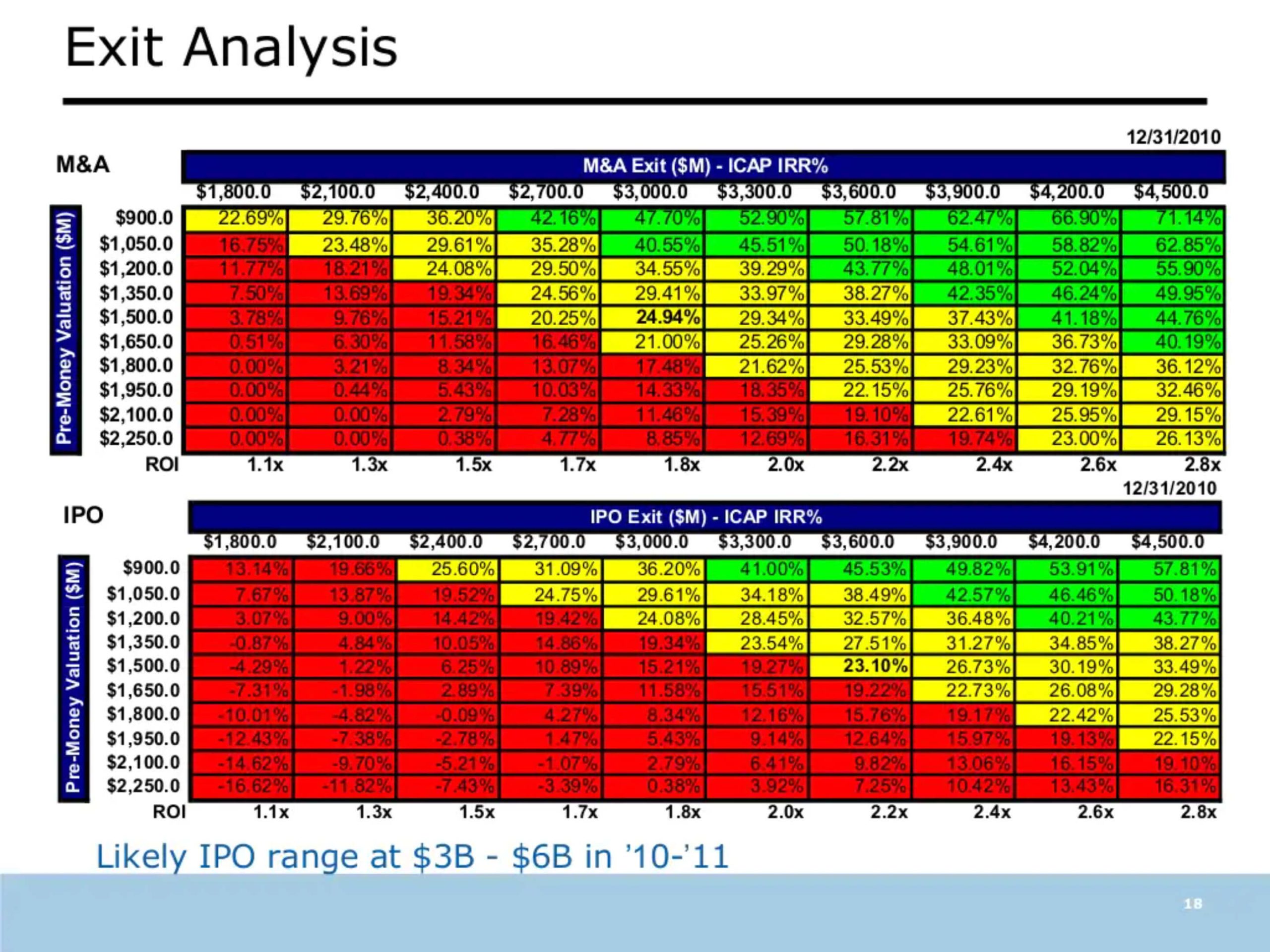

p.s. Separately, I cannot stress enough how prescient Reid was regarding optimizing for clean terms versus valuation. My competitive intel suggested that he got offers as high as $1.7b but they came with weird preference waterfalls, redemption clauses, and mandatory dividend payouts. He did a clean deal at $1.1b. Bain Capital won the lottery and look where it landed them.

About LinkedIN

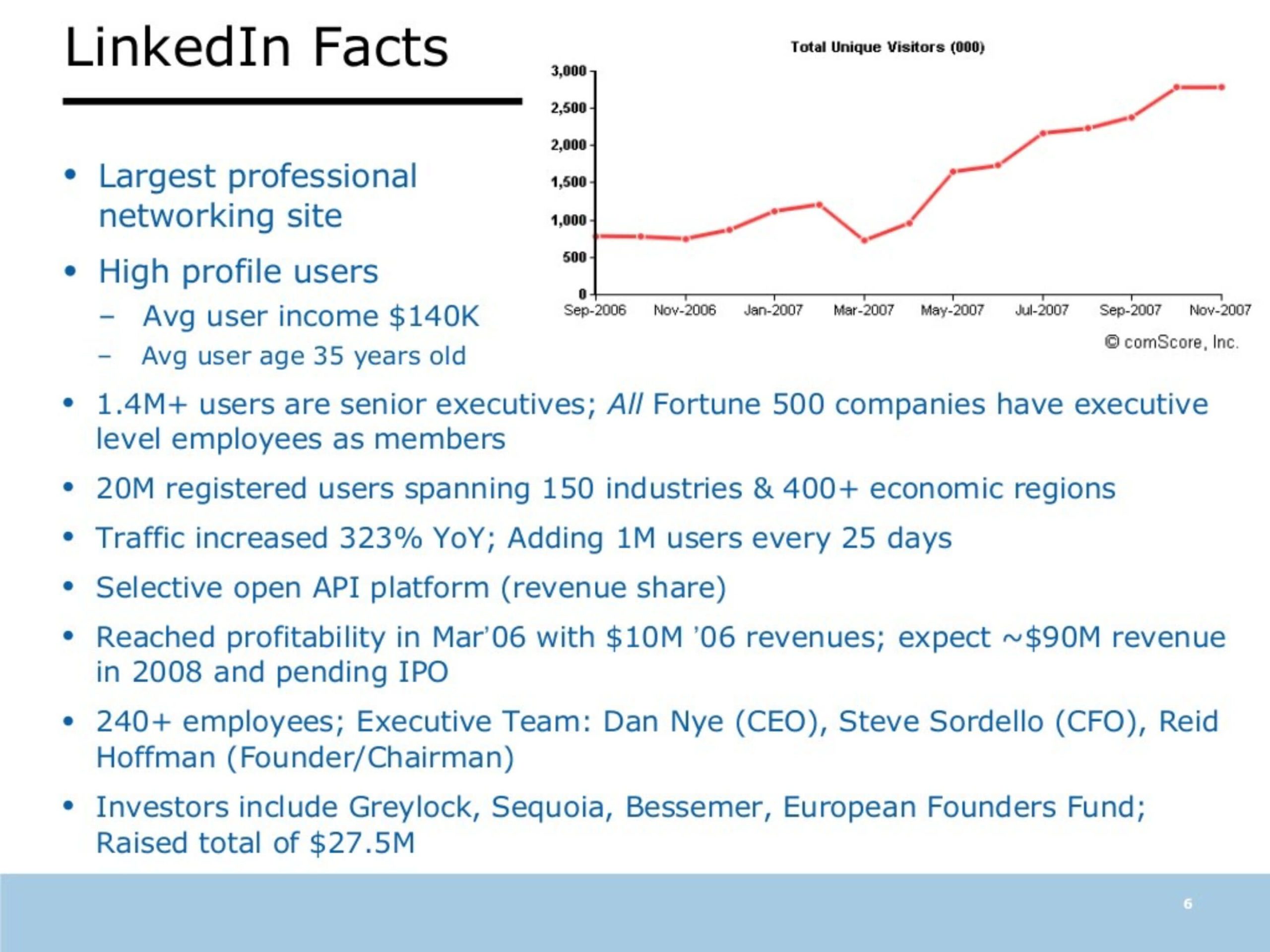

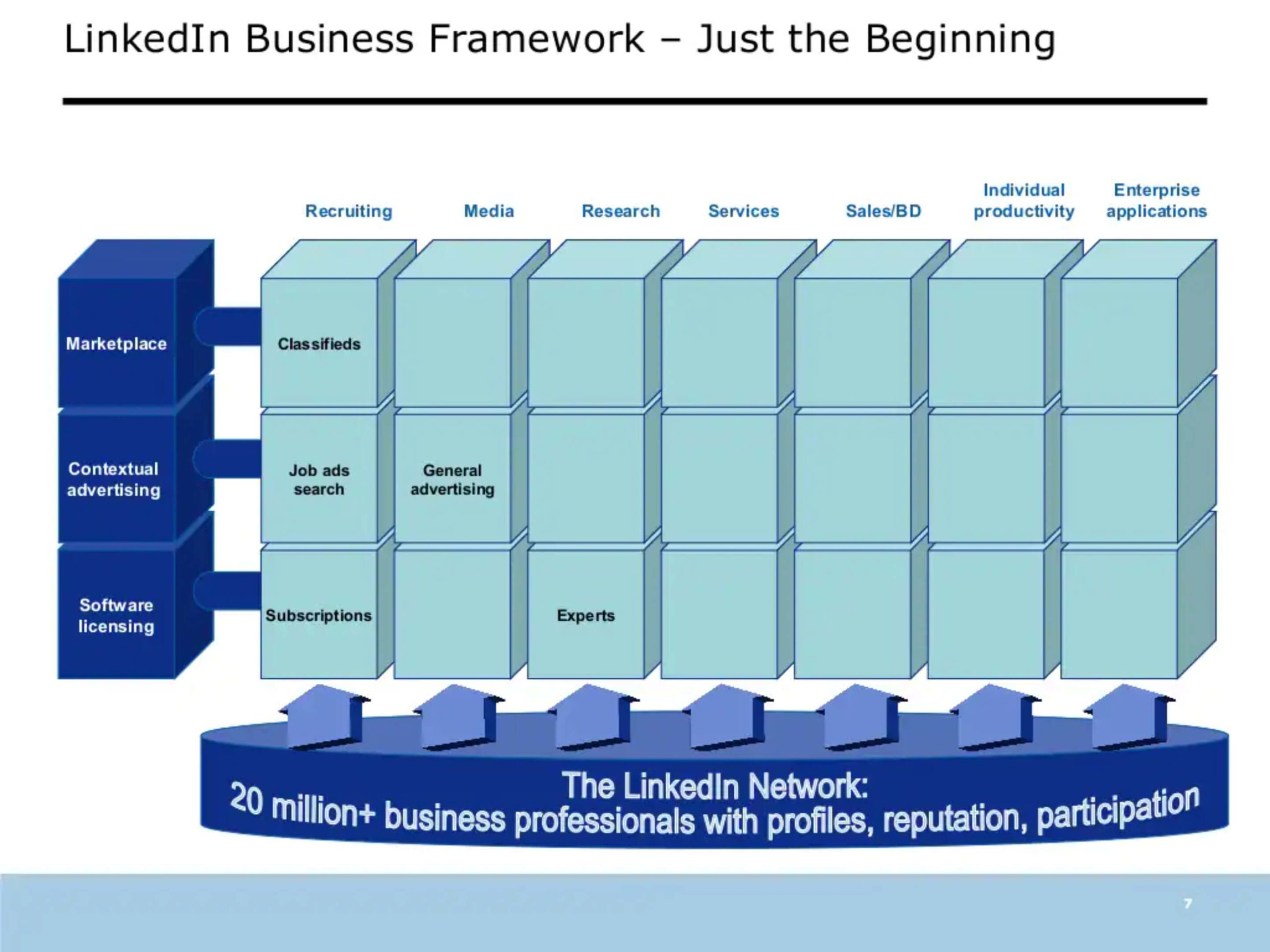

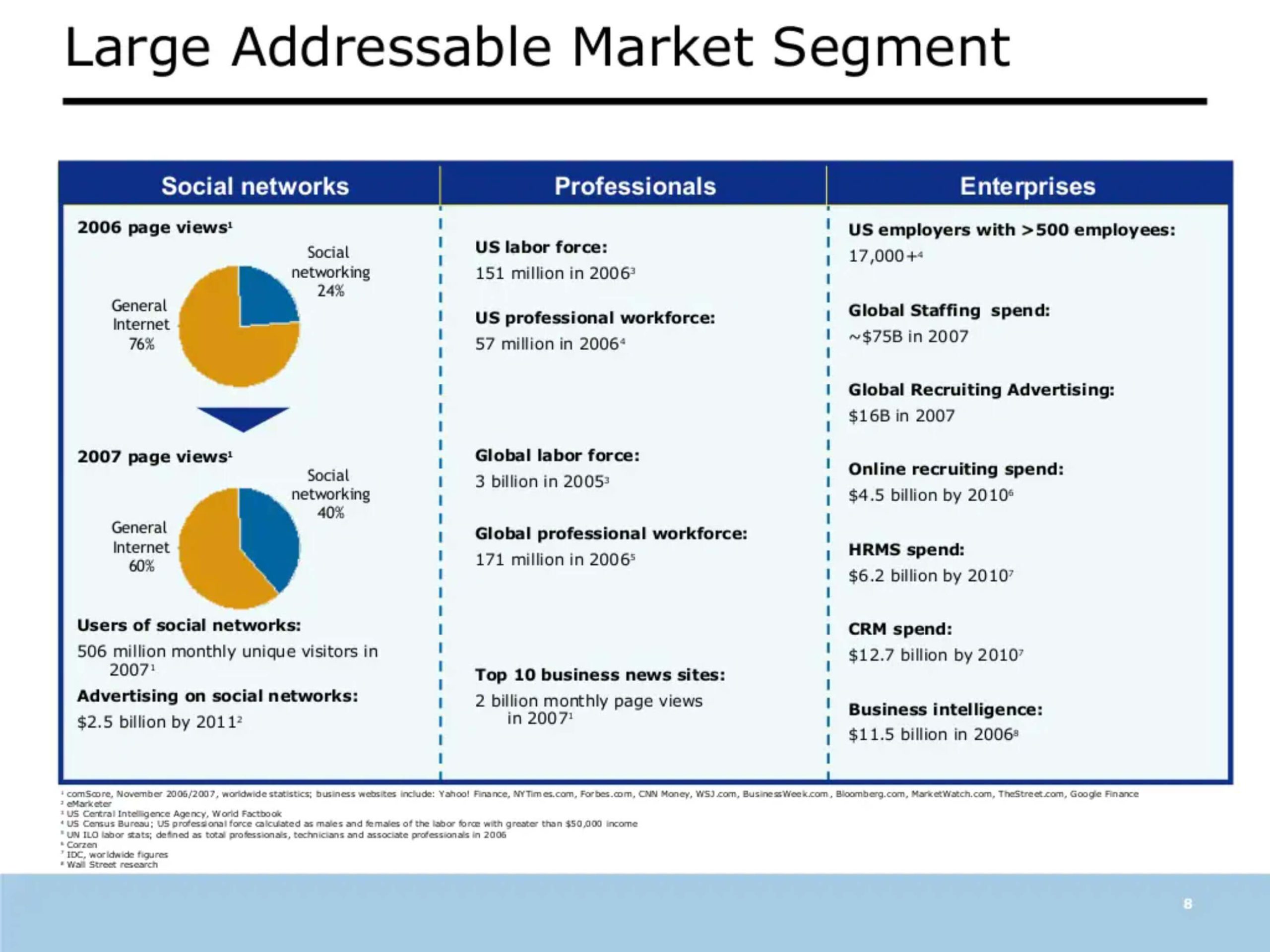

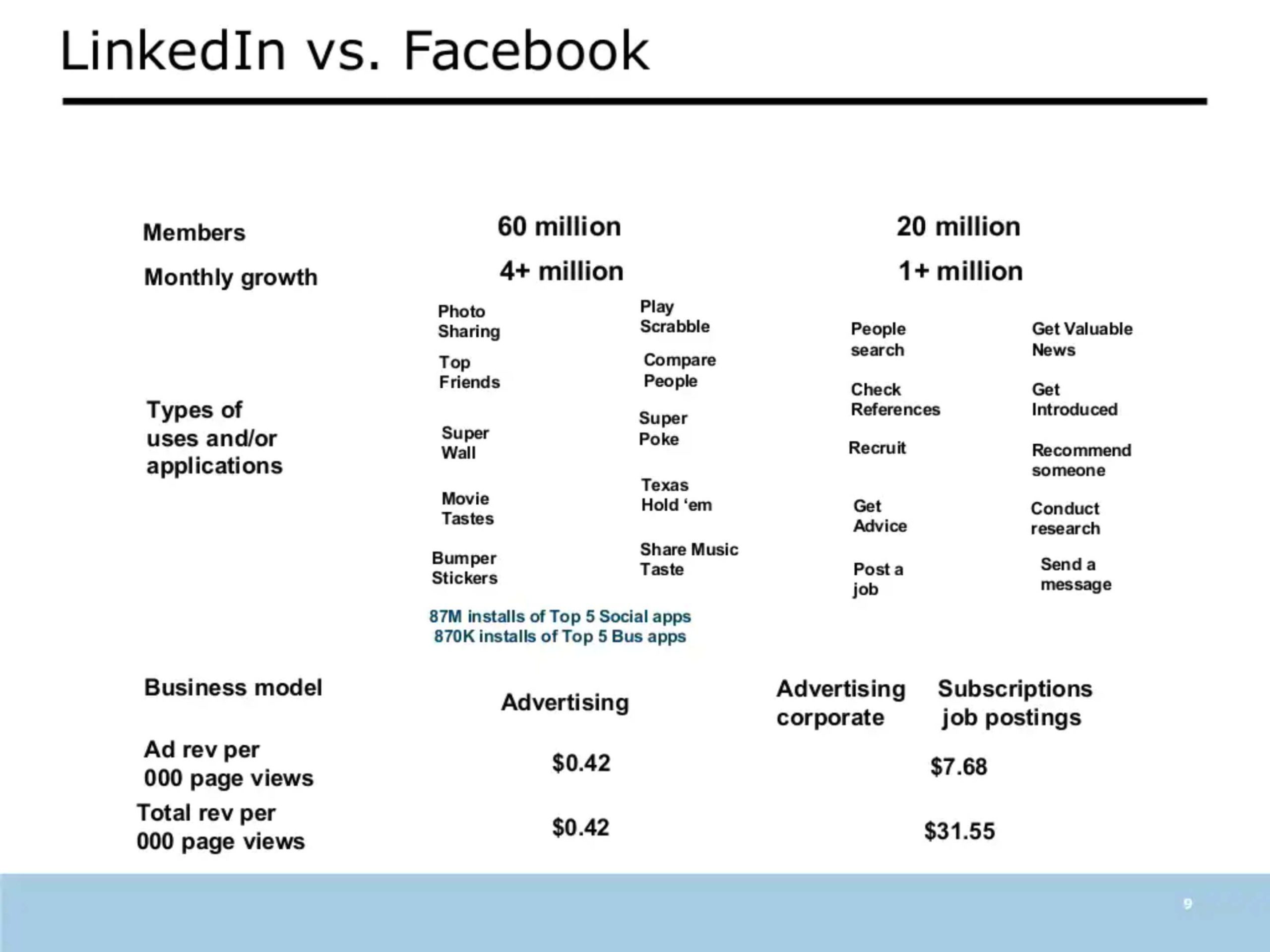

For those living under a rock, here is a reminder of what Linkedin is…

LinkedIn is a professional networking site that allows its members to create business connections, search for jobs, and find potential clients.

The site also enables its users to build and engage with their professional networks; access shared knowledge and insights, and find business opportunities. It offers LinkedIn mobile applications across

various platforms and languages such as iOS, Android, Blackberry, Nokia Asha, and Windows Mobile; a public website that allows developers to integrate its content and services into their applications; and a set of embeddable widgets to allow web developers to include content from the company’s network into their websites and applications.

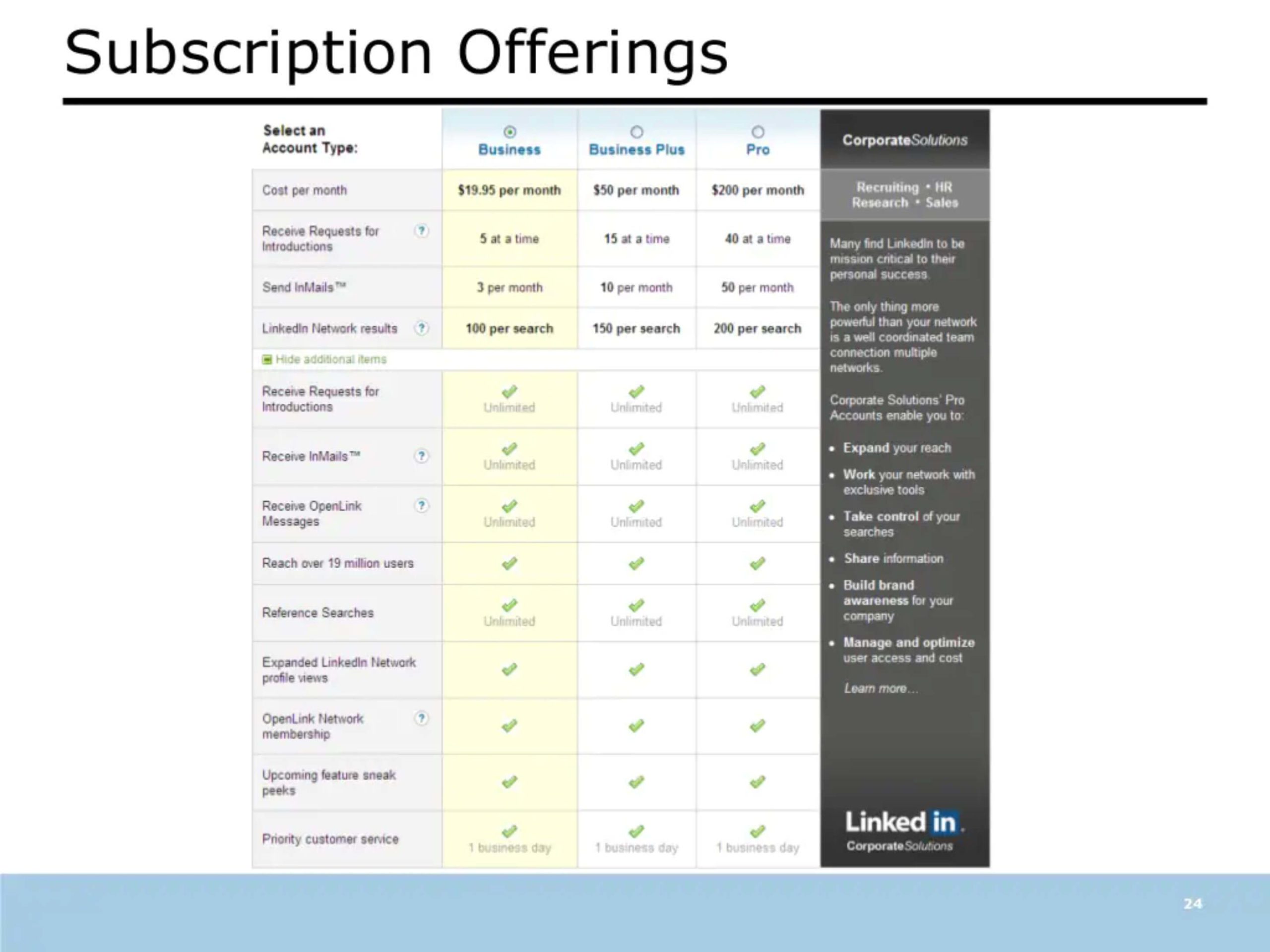

In addition, the company provides talent solutions, including LinkedIn Corporate Solutions that enables enterprises and professional organizations to find, contact, and hire qualified candidates; LinkedIn Jobs that allows enterprises and professional organizations to advertise job opportunities on the company’s network; and Subscriptions which enables recruiters and hiring managers to find, contact, and manage potential candidates. It also offers LinkedIn Ads, a self-service platform that enables advertisers to build and target their advertisements at its members; Enterprise, a marketing solution to target larger advertisers that receive dedicated account management and additional marketing solutions; and Sponsored Updates that enables advertisers to share and amplify content marketing messages.

Additionally, LinkedIn provides premium subscriptions for general professionals to manage their professional identities.

LinkedIn was founded in 2002 and is headquartered in Sunnyvale, California, United States.

About Intel Capital

Intel Capital invests in innovative startups targeting cloud and AI infrastructure, edge, 5G, autonomy, cybersecurity, client & gaming, enterprise applications, silicon design & manufacturing, and a wide range of other disruptive technologies. Since 1991, Intel Capital has invested US$12.9 billion in more than 1,582 companies worldwide.

When Eghosa tried to get in the deal, it was at the Series-D stage. CrunchBase is not reliable. I don’t know if that round was opened again, or it’s multiple reporting from VCs.

|

Announced Date

|

Transaction Name

|

Number of Investors

|

Money Raised

|

Lead Investors

|

| Feb 15, 2016 |

Post-IPO Equity – LinkedIn

|

1 | — | — |

| Jan 1, 2015 |

Secondary Market – LinkedIn

|

1 | — | — |

| Dec 1, 2009 |

Secondary Market – LinkedIn

|

1 | $51.6M | — |

| Oct 22, 2008 |

Series D – LinkedIn

|

4 | $22.7M | — |

| Jun 17, 2008 |

Series D – LinkedIn

|

4 | $53M | Bain Capital Ventures |

| Jan 29, 2007 |

Series C – LinkedIn

|

3 | $12.8M | Bessemer Venture Partners, Global Founders Capital |

| Oct 1, 2004 |

Series B – LinkedIn

|

1 | $10M | Greylock |

| Nov 1, 2003 |

Series A – LinkedIn

|

2 | $4.7M | Sequoia Capital |

Usual caveats

No investment memo made voluntarily public will ever be 100% as it was. The pressure is just too high for VCs to look smarter, and not make founders uncomfortable, etc. I highly praise the VCs that share their thought leadership so we can all learn.

If you’re learning to make a VC investment memo, don’t assume the memos are what you exactly need to do. Information will be redacted. Assume anything “delicate” or sensitive is not in the memos.

The only memo that is 1 to 1 is the Youtube memo because it was in a lawsuit.

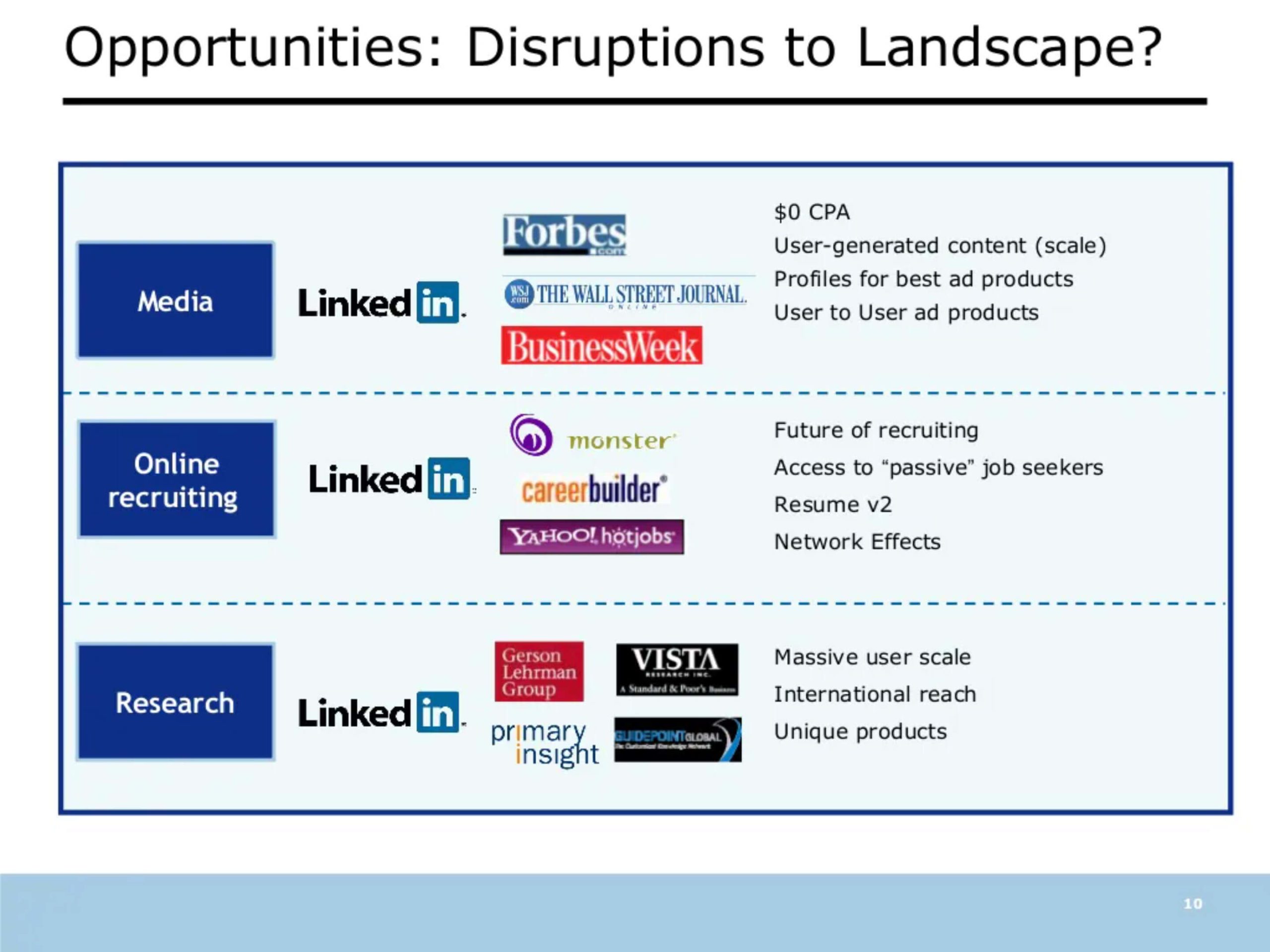

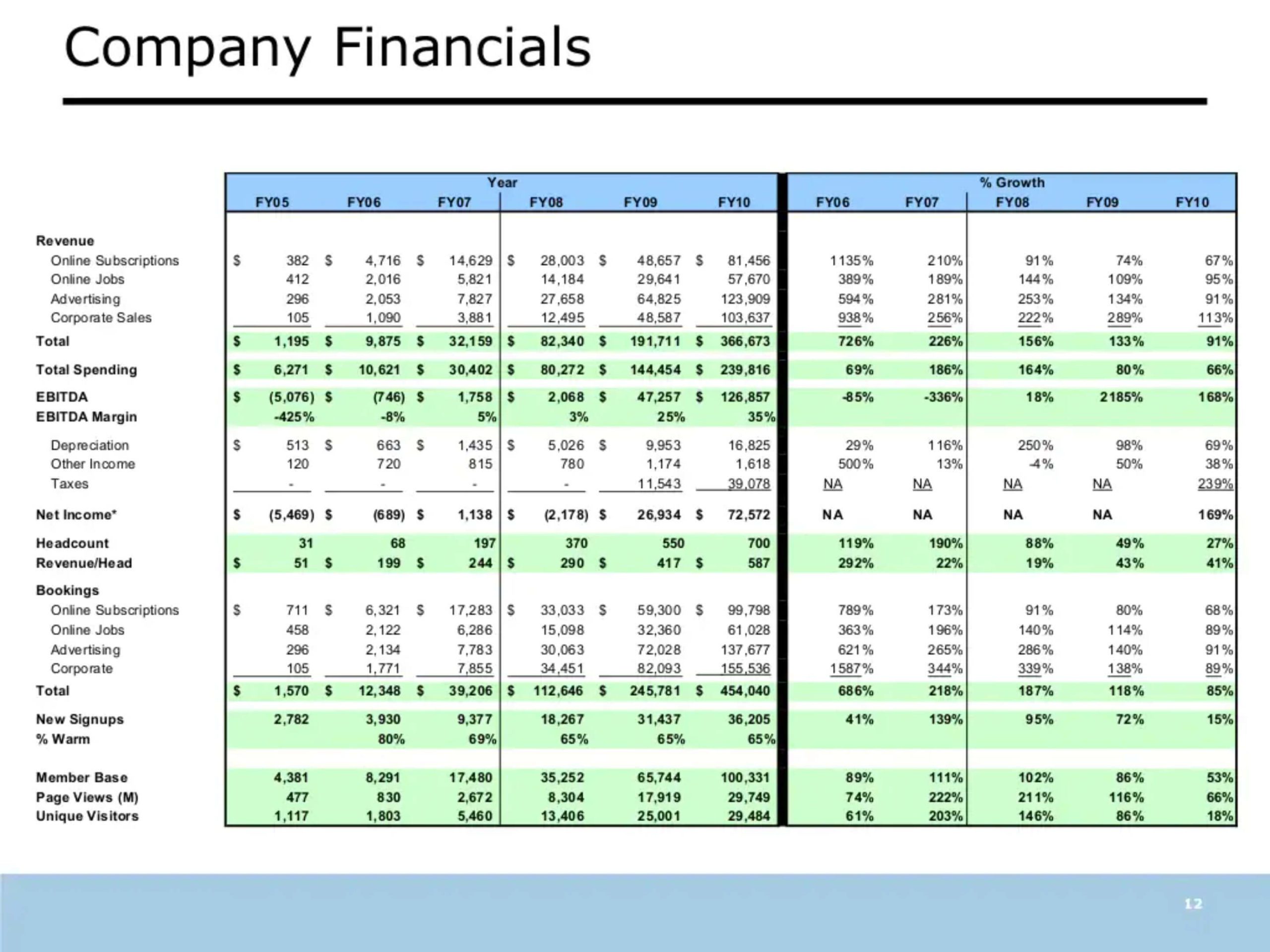

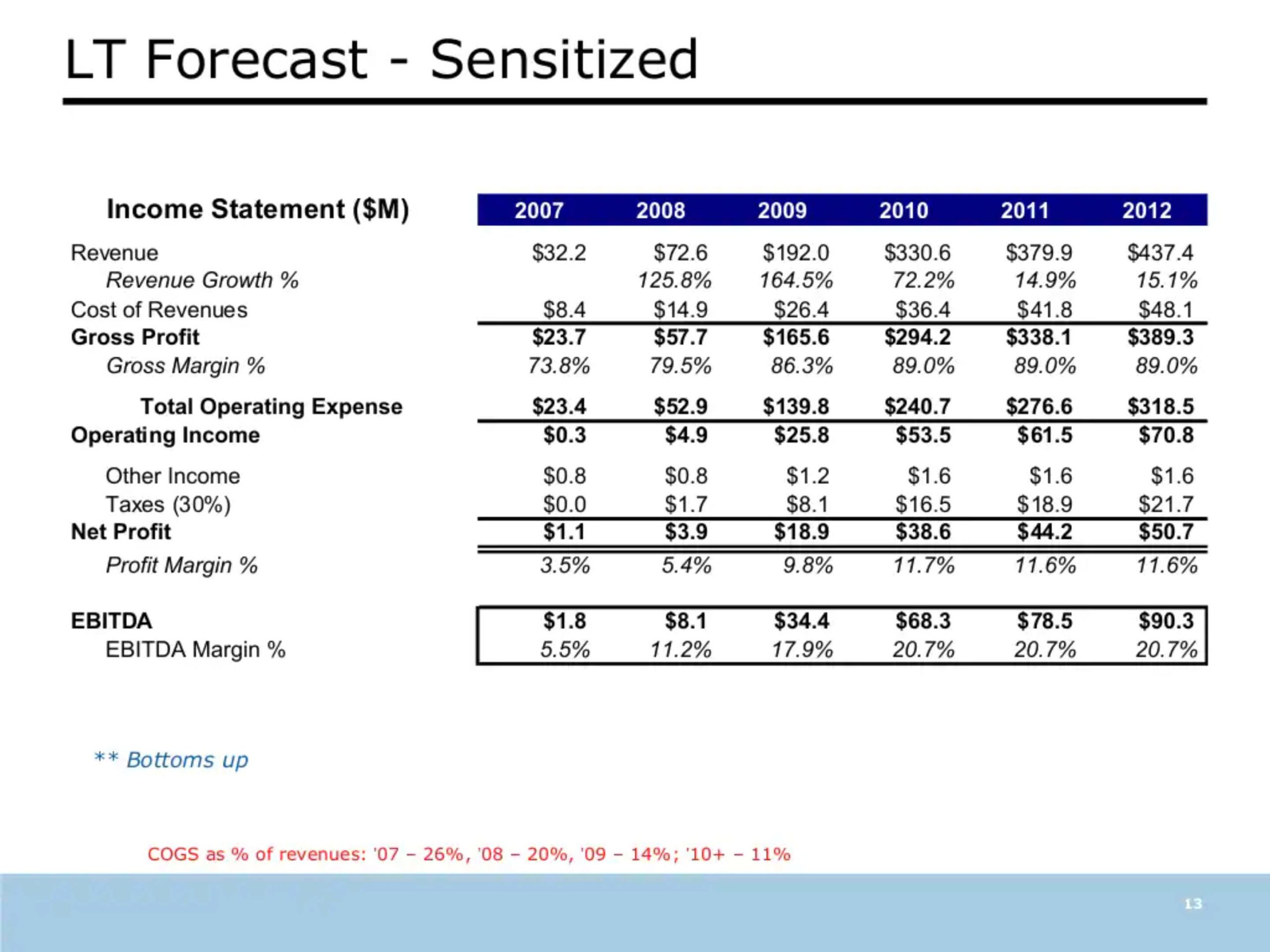

Venture Capital Investment Memo